Distributed Energy Resources Integration: Why DER Programs Die in the Middleware, Not the Hardware

Distributed energy resources integration is the discipline that decides whether the energy transition’s most impressive procurement numbers ever become operating capacity. The United States is adding distributed energy resources (DERs) — rooftop solar, batteries, smart water heaters, EV chargers — faster than at any point in grid history, and Lawrence Berkeley National Laboratory has published an entire integration framework because the bottleneck has moved. It is no longer panel supply or battery cost. It is the software layer between the asset and the market: the protocols, gateways, headends, and data models that let a million small machines act like one dependable resource. Hardware gets financed and delivered on schedule. Programs stall in the middleware, where the integration work was scoped last and thinnest.

Key Takeaways

- DER program failure is concentrated in the communication and control layer, where protocol choices, gateway ownership, and data models get decided too late.

- Battery storage is the stress test of DER integration: bidirectional, market-coupled, and state-constrained. An architecture that handles BESS handles everything else.

- Interconnection rules — California Rule 21, IEEE 1547-2018, FERC Order 2222 — have turned integration capability from an engineering preference into a market-access requirement.

- The binding constraint on the DER decade is integration capacity: teams that treat it as a product, with owned components and certified protocol layers, ship programs that work.

Distributed Energy Resources Integration Is a Protocol Problem Wearing an Infrastructure Label

Utilities and program operators tend to budget DER integration as if it were electrical work: an interconnection study, a meter swap, a commissioning visit. The harder and more consequential work is invisible from the substation. Every DER program lives or dies on a chain of communication seams, and each seam has a protocol decision attached.

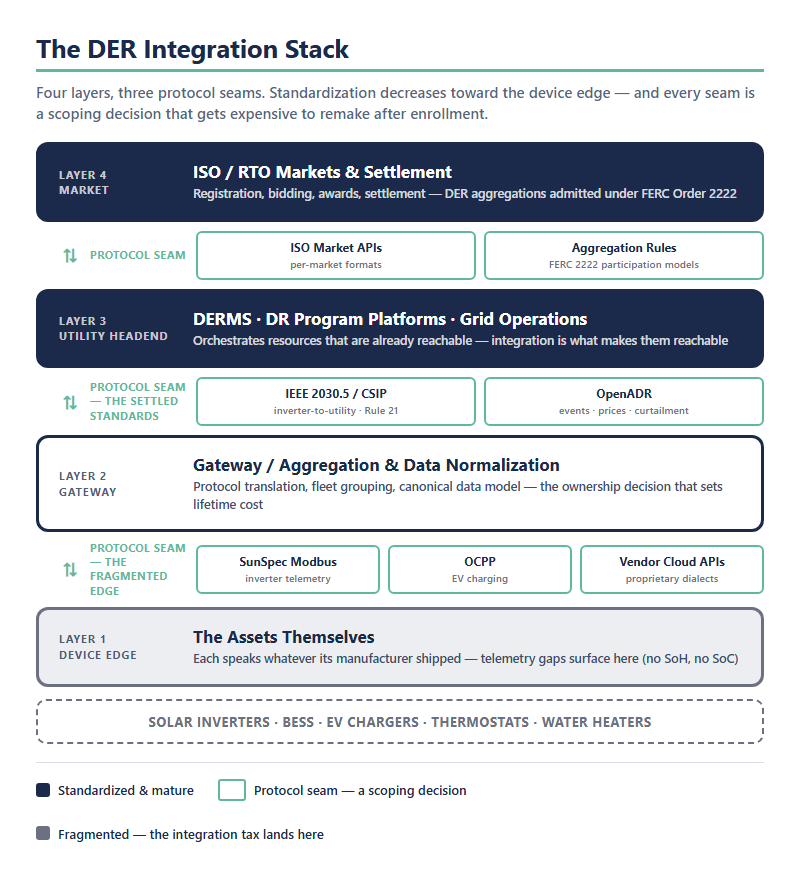

At the device edge, the asset speaks whatever its manufacturer shipped: SunSpec Modbus for inverters, proprietary cloud APIs for consumer batteries and thermostats. One level up, a gateway or aggregation platform translates those dialects into something a utility can use. The utility-facing seam is where the standards battle has largely been settled in favor of two protocols we work with daily: IEEE 2030.5, the smart-grid communication standard that California’s interconnection rules made the de facto national grammar for inverter-to-utility communication, and the OpenADR demand-response protocol, which carries program signals — events, prices, curtailment requests — between utilities, aggregators, and devices. Above that sit the market seams: ISO interfaces, settlement systems, registration platforms.

| Layer | What lives there | The protocol seam | Where it fails |

|---|---|---|---|

| Market | ISO/RTO interfaces, registration, settlement | ISO market APIs, FERC Order 2222 aggregation rules | Settlement formats that don’t reconcile with device telemetry |

| Utility headend | DERMS, DR program platforms, grid operations | IEEE 2030.5 / CSIP (inverter communication), OpenADR (program signals) | Per-utility profile variances treated as edge cases |

| Gateway / aggregation | Protocol translation, fleet grouping, data normalization | Vendor cloud APIs ↔ standard protocols | Vendor-owned gateways that lock program changes to a third-party roadmap |

| Device edge | Inverters, batteries, chargers, thermostats | SunSpec Modbus, OCPP, proprietary firmware APIs | Fragmented dialects; telemetry gaps (no state of health, no SoC) |

Read the table bottom-up and a pattern emerges: the layers closest to the market are mature and standardized, while the seams closest to the device are fragmented and quietly expensive. That asymmetry is the integration tax, and it lands on whoever scoped the middleware last.

The Integration Decisions That Get Made Too Late: Data Models, Headends, and Who Owns the Gateway

Three architectural questions determine most of a DER program’s lifetime cost, and all three are routinely answered by default rather than by design.

Who owns the gateway? When the aggregation layer belongs to a device vendor, every future program change negotiates with that vendor’s roadmap. When it belongs to the program operator, onboarding a new device class is configuration work. The ownership question sounds commercial; it is actually architectural, because it decides where translation logic lives and who can change it.

Which data model wins? A DER program reconciles at least three vocabularies: the device’s native telemetry, the utility’s grid model, and the market’s settlement format. Programs that never designate a canonical data model accumulate translation debt at every seam — the same reading mapped four slightly different ways, discovered during settlement disputes.

Where does orchestration live? A distributed energy resource management system is the right answer for utility-scale, multi-asset-class orchestration, and our analysis of DERMS platform architecture covers that decision in depth. The integration layer underneath it is a different problem: a DERMS orchestrates resources that are already reachable; integration is the work of making them reachable, reliably, at fleet scale. Buying an orchestration platform and assuming the integration comes bundled is the most common seven-figure scoping error in this market.

None of these decisions is difficult to make early. All of them are punishing to remake after ten thousand devices are enrolled. That is the case for treating DER integration software as a first-class procurement item, scoped alongside the hardware rather than after it.

BESS: The Hardest DER to Integrate, and the Most Valuable Once You Do

If you want to know whether an integration architecture is real, point it at a battery. Solar is forecastable and one-directional. A water heater accepts a setpoint. Grid-scale and customer-sited battery energy storage systems (BESS) are different animals: bidirectional, market-coupled, and constrained by a state of charge that is itself an economic variable. Every integration seam gets harder. Telemetry must carry state of health, not just output. Dispatch must respect degradation economics, not just capacity limits. Settlement must attribute revenue across stacked programs, a problem we quantified in our work on merchant BESS economics in ERCOT.

That difficulty is exactly why storage anchors the integration argument. A BESS is the most valuable DER on the grid per connected kilowatt — it can absorb as well as inject, shift energy across hours, and serve ancillary markets solar cannot reach. The dispatch and control intelligence that converts that flexibility into revenue is the subject of our deeper analysis of energy storage software; the integration layer is what connects that intelligence to the physical world. An architecture proven against BESS integration — grid codes, market interfaces, SoC-aware telemetry — will absorb every simpler asset class without redesign. The reverse is emphatically untrue, and programs that validated their middleware on thermostats discover it at the worst possible time.

Common DER classes, ranked by integration difficulty:

- Smart thermostats and water heaters — setpoint control, one-way telemetry, mature programs

- EV chargers — schedulable load, standardized protocols, growing bidirectional ambitions

- Solar inverters — standardized telemetry and curtailment, one-directional flow

- Customer-sited batteries — bidirectional, aggregated, SoC-constrained

- Grid-scale BESS — bidirectional, market-coupled, degradation-priced, multi-program

Interconnection Rules as Forcing Functions: Rule 21, IEEE 1547-2018, and FERC Order 2222

Regulation has quietly removed the option of treating integration as a later phase. California Rule 21 made IEEE 2030.5 communication capability a condition of connecting a smart inverter at all. IEEE 1547-2018, now rolling through state interconnection rules, requires every new DER to support standardized communication interfaces — the technical foundation of a grid that talks back. FERC Order 2222 completes the arc: DER aggregations now have a legal right to participate in wholesale markets, which means the integration chain from device to ISO is the product, end to end.

The market consequence is visible in who wins certification-gated deals. When SolarEdge needed to connect its fleet across multiple Australian grid operators under CSIP-Australia, the engagement was a multi-DNSP IEEE 2030.5 integration — protocol implementation, conformance, and utility-by-utility variance handling delivered as one workstream. The pattern repeats across every regulated market: the asset is admitted to the grid by its hardware specs, but it is admitted to the market by its integration stack. Manufacturers and operators who internalize that sequencing stop losing quarters to retrofit engineering.

Integration Capacity Is the New Interconnection Queue

For a decade, the energy transition’s binding constraint was the interconnection queue — gigawatts of willing capacity waiting on grid studies. For distributed resources, the constraint has shifted to something more tractable and more neglected: integration capacity, the ability to connect, control, and settle DERs faster than the program pipeline grows. Teams that treat integration as a product — owned gateways, a canonical data model, certified protocol implementations rather than one-off adapters — compound that capacity with every device class they add. Pre-certified components like our IEEE 2030.5 accelerator exist precisely to make the standardized seams a six-week implementation instead of a year of firmware archaeology, so the engineering budget concentrates where it differentiates. The DER decade will be won by the organizations that can absorb its hardware. That is a software race, and it is already underway.

Frequently Asked Questions

Distributed energy resources (DERs) are small-scale electricity assets located at or near the point of consumption rather than at central plants: rooftop and community solar, battery storage, EV chargers, smart thermostats, water heaters, and standby generators. Individually they are modest; integrated and aggregated, they function as dispatchable grid capacity.

Common examples include rooftop solar inverters, residential and commercial battery energy storage systems, EV charging stations, smart thermostats and HVAC systems, grid-interactive water heaters, and small wind or combined-heat-and-power installations. The defining trait is location on the distribution grid and the ability to be monitored or controlled.

Integrated DERs reduce peak demand, defer transmission and distribution upgrades, provide ancillary services, improve resilience during outages, and let consumers monetize flexibility. The benefits scale with integration quality: an unconnected DER serves only its host, while a well-integrated fleet bids into wholesale markets under FERC Order 2222 as a single aggregated resource.

Distributed generation refers specifically to electricity production at the edge of the grid, such as rooftop solar or small turbines. Distributed energy resources is the broader category: it includes distributed generation plus storage, controllable loads, and EV charging — assets that can consume, shift, or store energy as well as produce it. All distributed generation is a DER; most DERs today are something other than generation.

The utility-facing seams have converged on IEEE 2030.5 (smart inverter and DER-to-utility communication, mandated under California Rule 21 and spreading via IEEE 1547-2018 adoption) and OpenADR (demand-response event and price signaling). At the device edge, SunSpec Modbus dominates inverter telemetry, while EV charging adds OCPP. Most real programs run several of these simultaneously, which is why the gateway and data-model decisions carry so much weight.