How European DSOs Are Building DER Signaling Infrastructure

Five countries, four architecture patterns, and one question every grid operator will face by 2027

Every European DSO now accepts that distributed energy resources need to be signaled: curtailed, shifted, dispatched, and metered. But it’s 2026 and there is no single blueprint to follow.

Instead, what we get is a set of live experiments. The Netherlands has built the most complete protocol stack. Germany has built the most secure one. The UK has made the boldest regulatory commitment. The Nordics have the most mature market layer. France has taken a more pragmatic approach. This article maps out what each has built, and what architecture patterns are emerging. The point here is that the next DSO facing this decision can learn from five years of production deployments rather than starting from scratch.

Netherlands: OpenADR 3.0 for operations, Shapeshifter for markets

The Dutch approach is the clearest example of layered protocol architecture in Europe, and it is already in production.

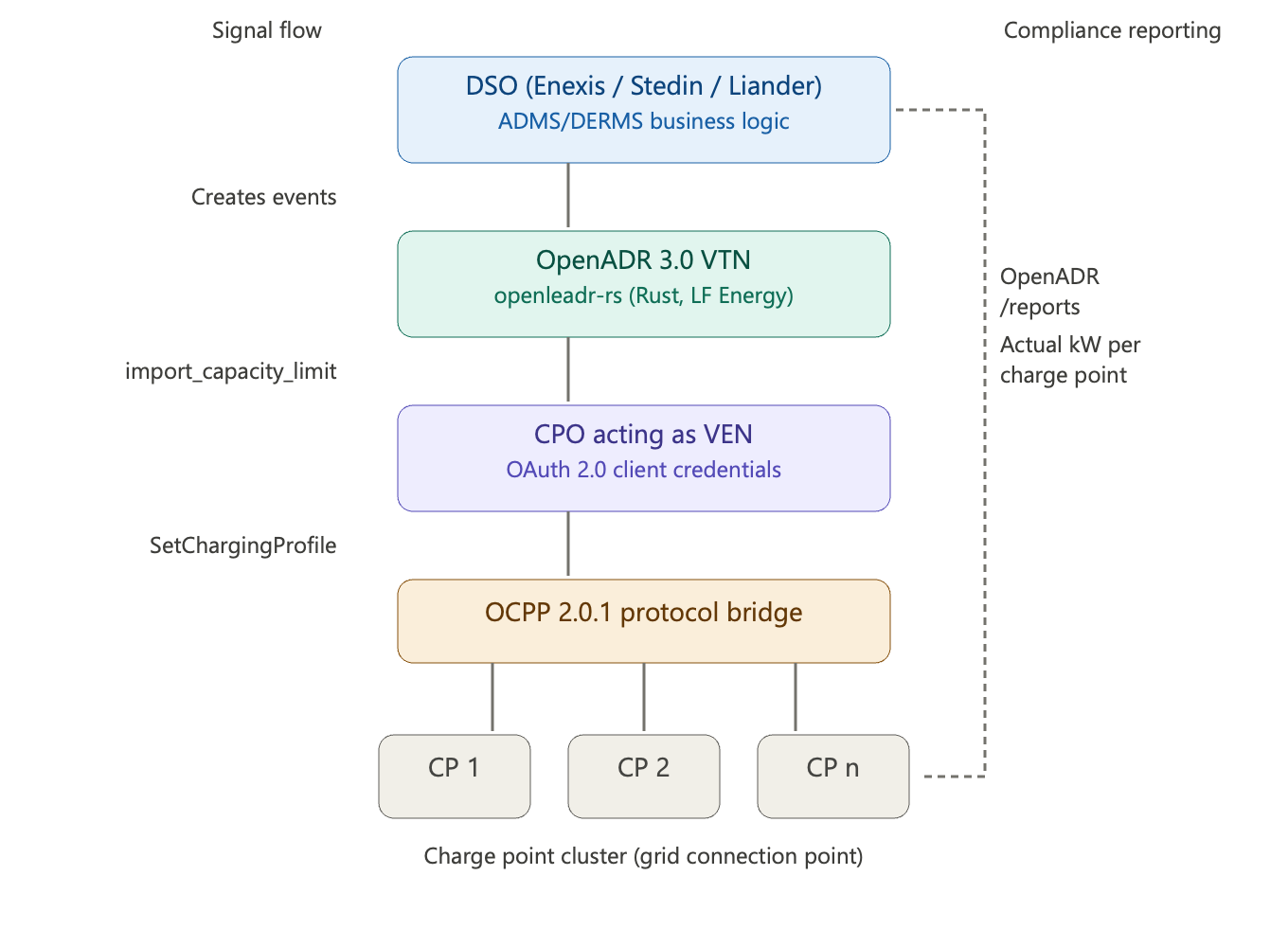

ElaadNL published version 2.0.0 of its Grid-Aware Charging specification in June 2025, built on OpenADR 3.0. DSOs (Enexis, Stedin, Liander) operate Virtual Top Nodes that send import_capacity_limit events to charge point operators connected as Virtual End Nodes. These are mandatory curtailment calls with binding capacity constraints. CPOs translate via OCPP SetChargingProfile to individual chargers and report compliance back through OpenADR’s /reports endpoint. As of early 2026, three DSOs and eight CPOs are running on the system, using the open-source openleadr-rs VTN/VEN (Rust, LF Energy, OAuth 2.0 authentication).

The Dutch innovation is the explicit separation between operational signaling and market-based trading. Above OpenADR sits Shapeshifter/UFTP, handling commercial flexibility on the GOPACS platform: FlexRequest → FlexOffer → FlexOrder → FlexOrderSettlement. OpenADR handles “reduce to X kW now.” Shapeshifter handles “I offer Y kW of flex at Z price for tomorrow.” This resolves a tension other markets still struggle with: the DSO needs deterministic real-time control for grid safety, but the market needs competitive voluntary participation for efficiency.

Germany: the SMGW fortress

Germany routes all DER control through the BSI-certified Smart Meter Gateway. Under §14a EnWG (mandatory since January 2024), controllable consumption devices above 4.2 kW must accept DSO signals via: DSO backend → SMGW → encrypted CLS channel → FNN Steuerbox → end device, using IEC 61850 for schedules and EEBUS for device control. Every node requires BSI TR-03109-5 certification. The architecture pattern underneath every national scheme — who owns the gateway, which data model wins — is mapped in our guide to distributed energy resources integration.

The security model is robust but slow. Germany’s smart meter rollout has reached approximately 10% of eligible households, accelerating under the revised Metering Point Operation Act (MsbG) but still far behind peers like Austria (97%) or the Netherlands. §14a also targets consumption-side flexibility only (heat pumps, EV chargers, batteries), leaving generation-side curtailment unaddressed. For DSOs whose primary challenge is solar feed-in congestion, the German model covers only half the problem.

United Kingdom: a single national dispatch standard

In March 2025, a Letter of Intent between ENA, Elexon, NESO, and the OpenADR Alliance confirmed OpenADR 3.1 as the unified dispatch API for all GB flexibility markets. This is the first European market to commit to a single protocol at a national regulatory level. Previous UK flexibility platforms (UKPN Flex, WPD Flexible Power, Northern Powergrid) each used proprietary APIs, creating integration burden for every flexibility provider. Elexon is now developing a “GB specification” within the OpenADR framework to collapse this fragmentation.

The UK’s commitment to 3.1 (not backward-compatible with 3.0) means implementations must account for enhanced object privacy, utility-assigned targets, and webhook subscriptions. The timeline for Elexon’s specification remains uncertain, but the directional signal is unambiguous.

Nordics: market-first via NODES

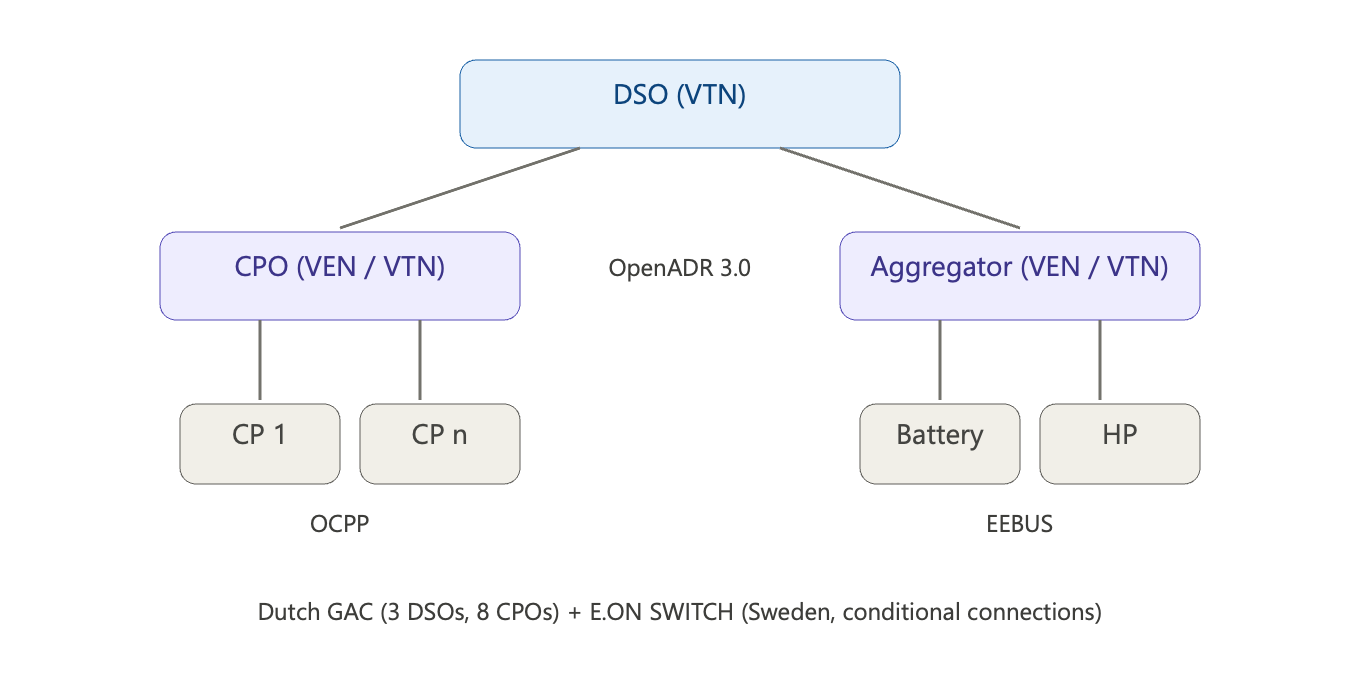

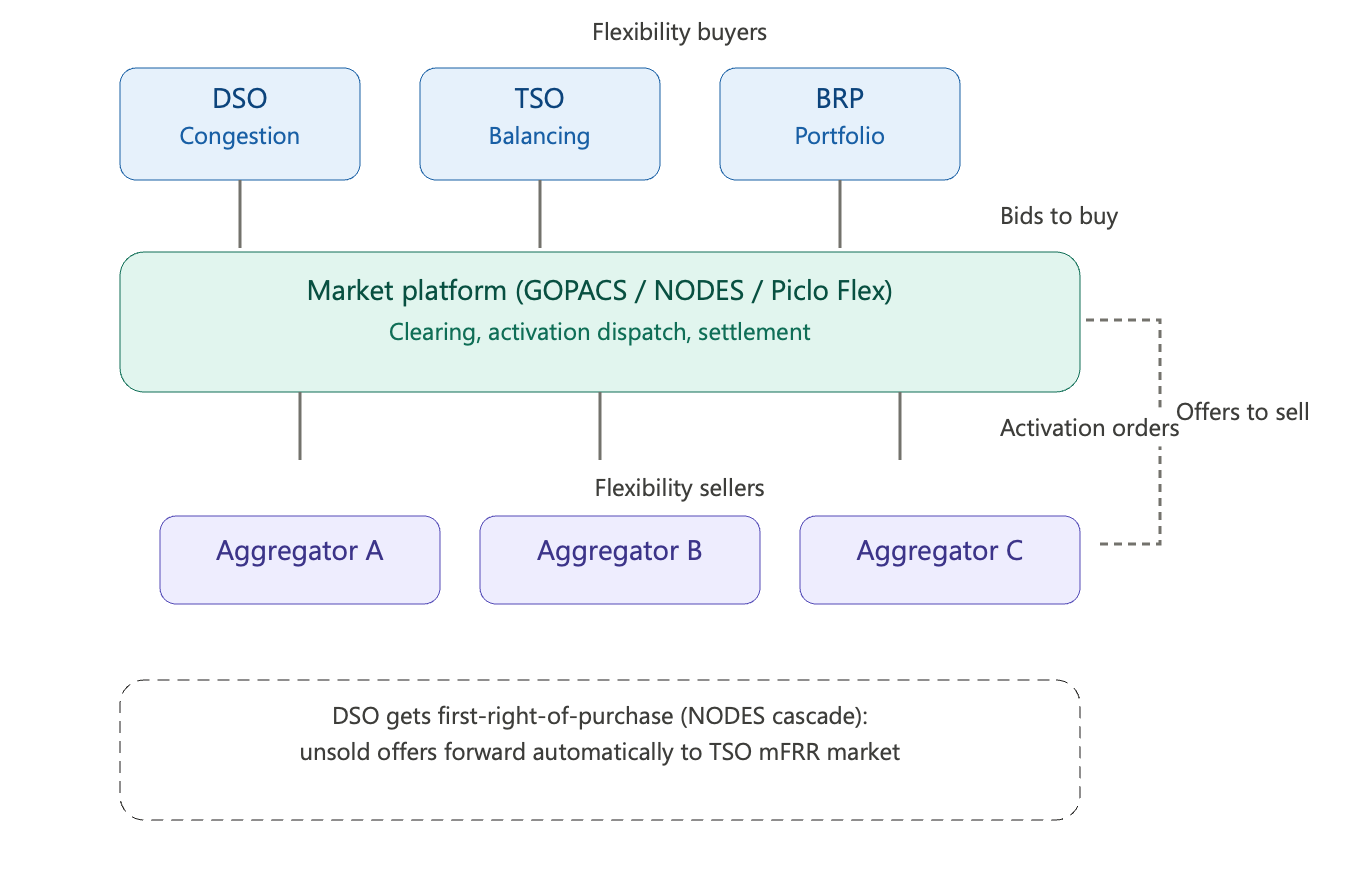

Norway’s NorFlex and Sweden’s sthlmflex operate on the NODES platform with standardized ShortFlex/LongFlex products. The key innovation: DSOs get first-right-of-purchase on flexibility bids until two hours before delivery. Unsold offers automatically cascade to the TSO’s mFRR balancing market, so one submission serves both local and system needs.

Sweden added a distinct contribution: E.ON’s SWITCH platform achieved the first OpenADR 3.0-certified VTN in March 2025, managing conditional grid connections where new generation accepts curtailment in exchange for faster, cheaper access. This is the first production use of OpenADR 3.0 for flexible grid connections anywhere in Europe.

France: pragmatic procurement

Enedis runs competitive tenders through its proprietary platform. It identifies constrained zones, issues tenders, and aggregators bid to provide services. Voltalis has won contracts for Paris and Lyon. The approach works because the number of counterparties is small and the interaction is procurement-style rather than real-time signaling. Whether the upcoming EU Network Code on Demand Response forces Enedis toward standardized protocols remains an open question.

| Country | Primary Protocol | Architecture Pattern | Maturity | Key Limitation |

|---|---|---|---|---|

| Netherlands | Signaling: OpenADR 3.0 Market: Shapeshifter/UFTP |

Layered: DSO as VTN (Pattern A) + GOPACS market (Pattern C) | Production (3 DSOs, 8 CPOs) | EV charging focus; broader DER coverage evolving |

| Germany | Signaling: IEC 61850 via SMGW Device: EEBUS |

Centralized security: BSI-certified gateway chain | Mandatory (§14a EnWG), ~10% rollout | Consumption-only; no generation-side curtailment |

| United Kingdom | Signaling: OpenADR 3.1 (committed) | National standard: single dispatch API for all GB flex markets | Regulatory commitment; spec in development | 3.1 not backward-compatible with 3.0; timeline uncertain |

| Nordics | Market: NODES platform Signaling: OpenADR 3.0 (Sweden) |

Market-first: DSO first-right-of-purchase, TSO cascade | Production (NorFlex, sthlmflex, E.ON SWITCH certified) | Market design strong; operational signaling layer varies |

| France | Procurement: proprietary Enedis platform | Tender-based: competitive procurement per constrained zone | Operational (Paris, Lyon contracts) | Proprietary; may need standardization under EU Network Code |

Four architecture patterns are consolidating

Pattern A: DSO as VTN, direct to aggregators/CPOs. The DSO runs an OpenADR VTN and sends operational commands to VENs that can cascade downstream to devices. Dutch GAC and Swedish SWITCH exemplify this. Best for non-negotiable curtailment and capacity limits.

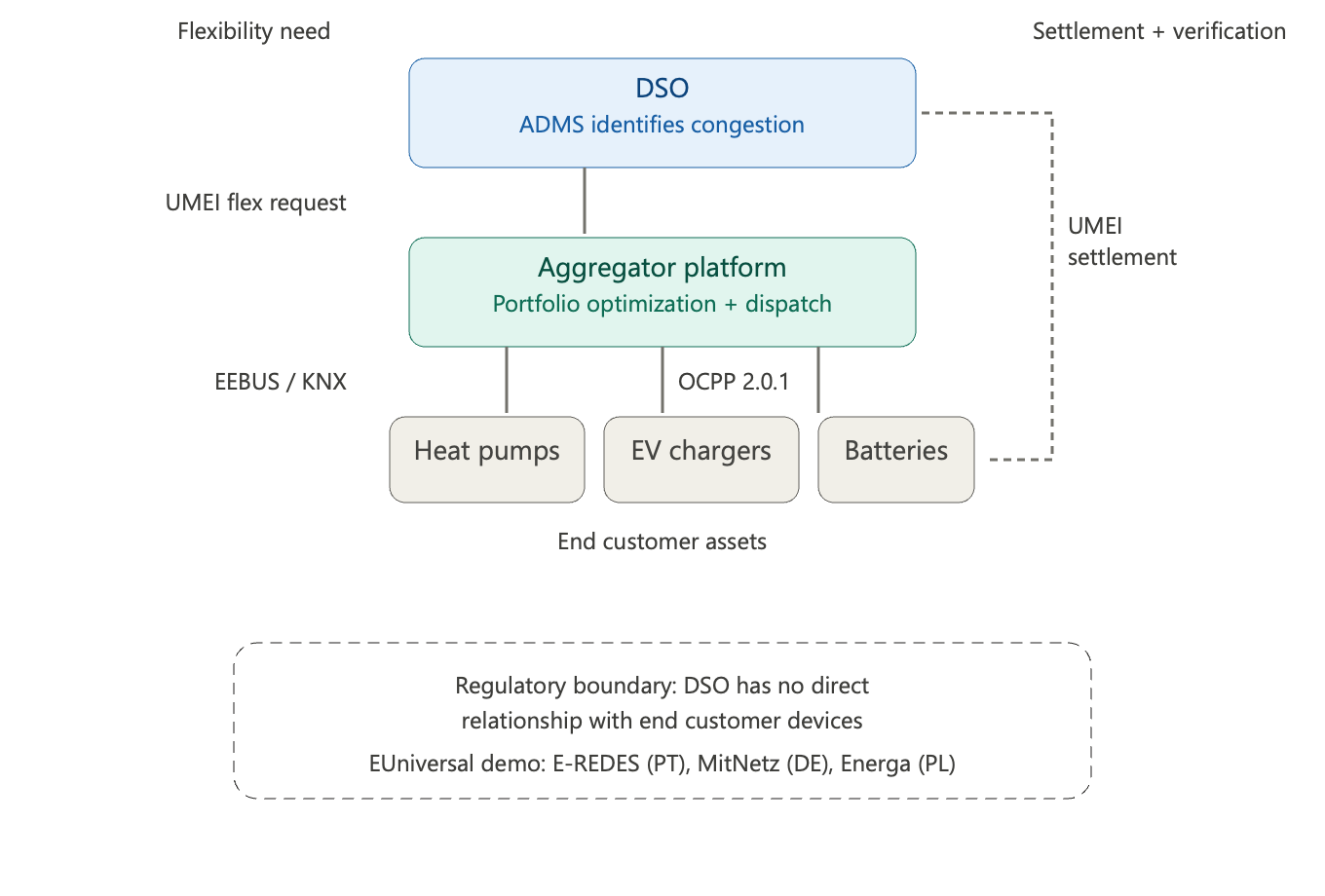

Pattern B: DSO → aggregator platform → devices. The DSO communicates flexibility needs via API to aggregators who translate to device protocols. Respects regulatory separation between DSO and end customer. Demonstrated in EUniversal across Portugal, Germany, and Poland.

Pattern C: Market platform mediates. An independent market (GOPACS, NODES, Piclo Flex) handles clearing and settlement between multiple buyers and sellers. Best where DSO, TSO, and BRPs compete for the same resources.

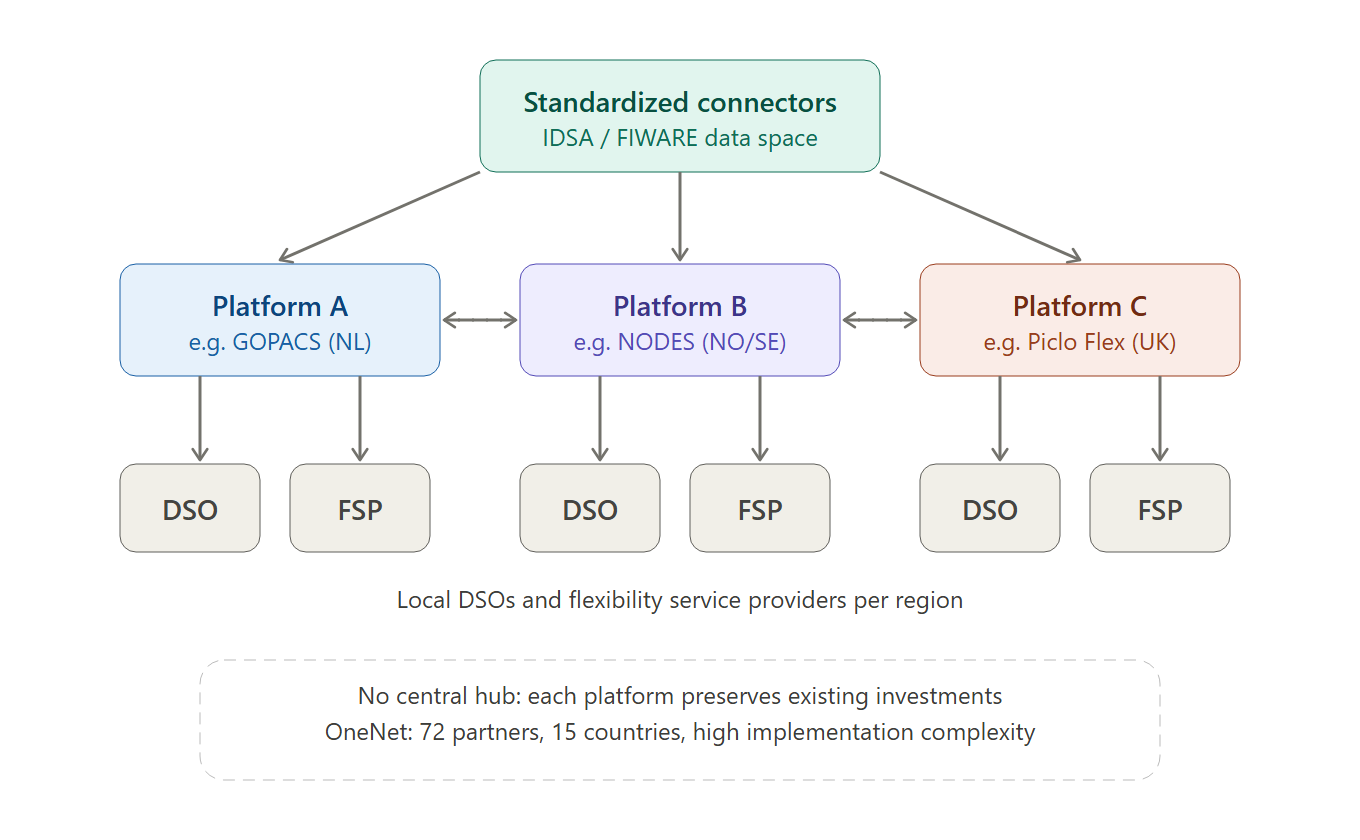

Pattern D: Hybrid network-of-platforms. The long-term EU target from OneNet: decentralized platforms connected via standardized connectors. Conceptually elegant, implementation complexity high.

Most DSOs will need a combination. The Dutch system already demonstrates this: Pattern A (OpenADR for operational signals) coexisting with Pattern C (GOPACS/Shapeshifter for market transactions).

The interoperability stack

No single protocol covers the full chain. The emerging architecture has four layers: CIM (IEC 61968/61970) for TSO-DSO coordination, OpenADR for DSO-to-aggregator signaling, market protocols (Shapeshifter, UMEI, platform APIs) for commercial trading, and device protocols (OCPP, EEBUS, Modbus/SunSpec, S2) for the last mile. The bridges between layers, especially OpenADR-to-OCPP, are where most integration time and budget concentrate. Hamburg’s Project ELBE validated this bridge across 8 CPOs, 17 charger types, and 28 substation areas.

CEN-CENELEC’s April 2025 standards list for demand response, which feeds into the EU Network Code expected enforceable around 2027, explicitly includes OpenADR, OCPP, S2, IEC 61850, and CIM. DSOs will need to demonstrate compliance with these standards alongside their own interfaces.

Start With What Works, Iterate Toward What Scales

The protocol question is converging. OpenADR 3.0/3.1 has achieved production deployment (Netherlands), regulatory adoption (UK), certified products (Sweden), and CEN-CENELEC inclusion. For DSO-to-aggregator signaling, the trajectory is clear.

Architecture matters more than protocol. Who operates the VTN, how it integrates with your ADMS, whether you cascade through aggregators, how you bridge to device protocols: these choices drive most implementation complexity.

The Dutch model offers the fastest path. ElaadNL went from specification to three DSOs and eight CPOs in roughly 18 months. The stack is open-source, Docker-deployable, and publicly documented.

Design for security from day one. NIS2 classifies energy entities as essential infrastructure. Building from scratch is an advantage, but only if security is concurrent with architecture rather than bolted on after the pilot.

Don’t wait for the perfect standard. The Dutch started with mandatory calls and are evolving toward markets. The UK committed before the spec was finished. Sweden certified a VTN before most of Europe had heard of OpenADR 3.0. The DSOs furthest ahead started with what was available and iterated.

Frequently Asked Questions

OpenADR 3.0 and 3.1 are emerging as the dominant DSO-to-aggregator signaling protocols across Europe. The Netherlands uses OpenADR 3.0 in production for grid-aware charging, the UK has committed to OpenADR 3.1 at a national regulatory level, and Sweden achieved the first certified OpenADR 3.0 VTN in Europe. Germany is the notable exception, routing DER control through BSI-certified Smart Meter Gateways using IEC 61850.

The Dutch system uses a layered architecture: DSOs operate OpenADR 3.0 Virtual Top Nodes that send capacity limit events to charge point operators acting as Virtual End Nodes. CPOs translate these signals to individual chargers via OCPP SetChargingProfile commands. Above the operational layer, the Shapeshifter/UFTP protocol handles commercial flexibility trading on the GOPACS platform. This separation ensures deterministic grid safety controls coexist with competitive market participation.

Operational signaling (e.g., via OpenADR) delivers mandatory, real-time commands from DSOs to devices — “reduce to X kW now.” Flexibility markets (e.g., via Shapeshifter or NODES) enable voluntary, price-based trading — “I offer Y kW at Z price for tomorrow.” Most mature European systems separate these functions into distinct protocol layers because they serve fundamentally different purposes: grid safety versus economic efficiency.

The Netherlands leads in production deployment maturity. ElaadNL’s Grid-Aware Charging specification went from publication to three DSOs and eight CPOs in roughly 18 months, using an open-source, Docker-deployable stack. The UK leads in regulatory ambition with its national commitment to a single dispatch standard. Sweden leads in certified interoperability with Europe’s first OpenADR 3.0-certified VTN.

CEN-CENELEC’s April 2025 standards list, which feeds into the EU Network Code expected to be enforceable around 2027, explicitly includes OpenADR, OCPP, S2, IEC 61850, and CIM. DSOs will need to demonstrate compliance with these standards, making early adoption of recognized protocols a strategic advantage rather than just a technical preference.