eMSP vs CPO: Roles, Revenue Models, and When the Operator Has to Run Both

eMSP vs CPO is usually framed as a definitional question — what an e-Mobility Service Provider does, what a Charge Point Operator does, and which role does what in an EV charging session. The piece sitting on the SERP today answers that question and stops there. The operator’s question is different. Should the business run one role, the other, or both, given the revenue model of each, the regulatory forcing functions reshaping the role boundary, and the integrated-stack arbitrage now available at the OCPI settlement layer between them? Increasingly, the answer points to cpo and emsp joint solutions — integrated-stack platforms that put charge-point management and driver-side eMSP functions on one operator-owned codebase. This guide walks the role-and-revenue decision an operator should run before committing to a single-role platform strategy in 2026. The four-lever eMSP platform investment thesis sets the strategic frame; this piece walks through the role boundary that decides which lever the operator actually pulls.

Why “eMSP vs CPO” Is a Decision Question, Not a Definition Question

The SERP for cpo vs emsp answers the definition. Most vendor explainers lead with “both eMSPs and CPOs are essential to EV charging,” list five or six role differences, and stop. The piece is correct and useless to the operator who has to commit capital to one or both roles inside the next planning cycle.

Five forcing functions are reshaping the role boundary between 2024 and 2028, and each one pulls the roles closer together rather than keeping them apart. AFIR enforcement imposes cross-role data and payment obligations: the CPO publishes real-time station data and contactless payment at the charger; the eMSP exposes ad-hoc charging without a Tokens-authenticated session. ISO 15118-20 plug-and-charge spans both sides — contract certificates handled by the charger and back-end settlement handled by the driver-side platform. OCPI 2.2.1 hub maturity raises the depth bar on the contractual surface between CPO and eMSP. V2G market entry in the UK, NL, and DE requires both physical asset control and driver-side settlement on the same transaction. And FERC Order 2222 plus the EU CER aggregation framework position the operator that runs both as a potential aggregator counterparty in wholesale markets.

The shift the operator has to absorb is not philosophical. Five years ago, eMSP and CPO were complementary specializations served by different vendors. Today, the integrated stack captures revenue and regulatory positioning that the disaggregated model cannot. The operator’s question is no longer “which role does what?” — that is FAQ Q1 territory. The question is “should I run one, the other, or both, and which one starts?”

What an eMSP Owns That a CPO Cannot Own — and the Revenue That Comes With It

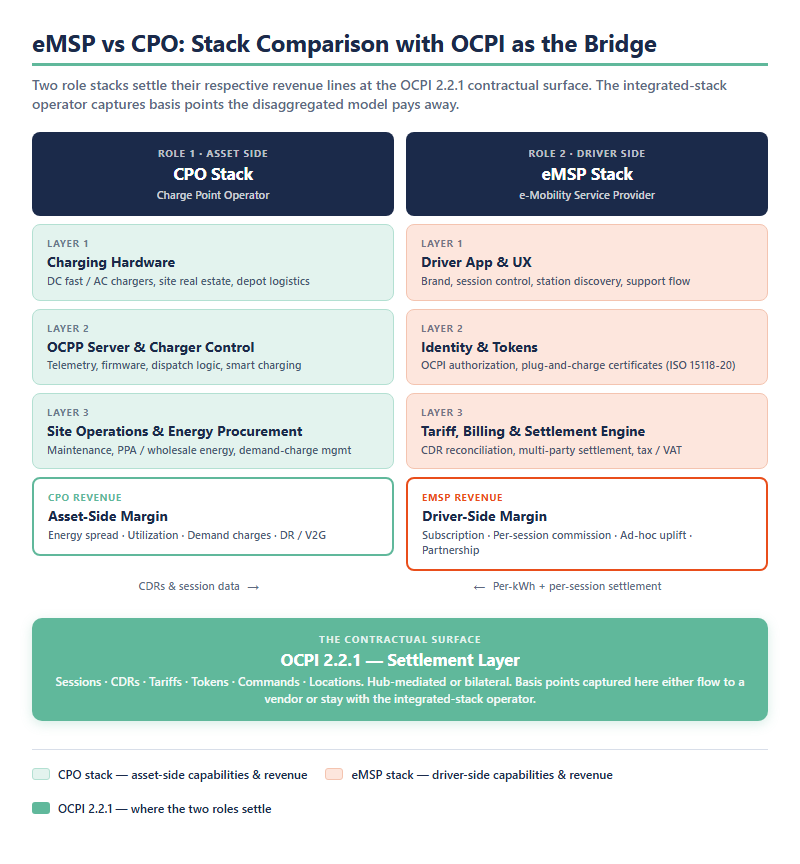

The eMSP owns the driver. Identity, roaming reach, in-app experience, billing visibility, support workflow, brand presence — every touchpoint a driver has with EV charging flows through the eMSP layer. The CPO can run a flawless physical network and never own a driver relationship if the eMSP captures the experience.

The emsp revenue model runs on driver-side margin. Subscription revenue covers the predictable cohort — B2C monthly plans, B2B fleet contracts with negotiated rates per driver. Per-session commission on roaming sessions captures the bilateral CPO traffic. Ad-hoc payment uplift — driven by AFIR’s mandatory contactless payment without account creation — is structurally higher-margin than the subscription cohort because the operator does not amortize acquisition cost across the relationship. Partnership revenue with corporate fleets, automaker companion programs, retail loyalty integrations, and utility-affiliated demand programs sits on top of all three.

The driver-side moat is durable. Drivers do not switch eMSPs once their charging history, payment, saved stations, and loyalty data are anchored on one platform — the migration friction is real and the substitution cost rises with relationship tenure. That is the structural reason emsp business model thinking starts with driver lifetime value, not with charger count. The eMSP’s job in the EV charging value chain is to own the part of the driver experience that compounds across years; emsp vs cpo as a procurement question presupposes that the eMSP side captures that compounding margin and the CPO side does not.

The audit question for an operator considering the eMSP role: do you have an existing driver relationship (or an obvious access path to one) to build on, and what is the lifetime value per driver in your target market? Operators with answers — automaker companion app teams, mobility retailers, utility-affiliated branded programs — start with the eMSP role and add CPO capabilities later. Operators without a path to driver relationship typically start CPO-side and add eMSP capabilities once the network has driver traffic.

What a CPO Owns That an eMSP Cannot Own — and the Revenue That Comes With It

The CPO owns the asset. Charging hardware in the ground, site real-estate (or long-tenure lease), energy procurement at the meter, OCPP-side charger control, maintenance economics, and depot logistics — every kilowatt-hour dispensed at scale touches the CPO layer. The eMSP can run a beautiful driver app and never own a charger if the CPO captures the asset side.

The cpo revenue model runs on asset-side margin. Energy spread between wholesale procurement (or PPA) and retail tariff is the primary line. Utilization economics — revenue per kWh dispensed per station per day — decides whether a depot or corridor pays back inside the planned horizon. Demand-charge management is material in US ISO-RTO markets where commercial tariffs penalize peak draw, and the CPO who controls the dispatch logic captures the savings. Ancillary grid services — DR enrollment, V2G dispatch revenue, frequency response — add a fourth line that the asset side captures and the driver side cannot.

The asset-side moat is durable in a different way than the driver moat. Charging hardware in the ground is capital-intensive and difficult to switch operator for, especially in markets with long-tenure site leases. The charge point operator role compounds at the physical layer rather than the relationship layer, and the cpo business model that wins long-term is the one that holds high-utilization sites on contracts measured in years, not quarters.

The audit question for an operator considering the CPO role: do you have access to capital, site-acquisition expertise, and operational discipline for a multi-million-dollar hardware build-out, and what is the network utilization in your target market? Operators with answers — utilities, large retail real-estate holders, fleet operators with private depots — start with the CPO role. The CPO-side platform companion walks through the platform layer that backs all of this; the parallel CPO-side white-label platform companion covers the buy-vs-build decision on the CPO side specifically.

Where the Revenue Models Meet — OCPI as the Contractual Surface Between Them

The eMSP captures driver margin. The CPO captures asset margin. The two revenue models meet at the OCPI 2.2.1 protocol architecture — the contractual surface where the eMSP’s per-session commission meets the CPO’s per-kWh tariff. Every charging session in 2026 settles through this surface, and the operator that runs both roles internally captures the basis points the disaggregated model pays away every transaction.

The economic surface is layered. Roaming hub fees (Hubject, GIREVE, eRoaming) absorb basis points at the long-tail partner count where bilateral OCPI agreements are not economic. Bilateral CPO agreements pay the operator back at strategic-partner volume — direct counterparty terms eliminate the hub layer’s spread on the highest-traffic connections. Settlement clocks decide how long the operator’s working capital sits between session and revenue recognition. Dispute workflow decides what happens when the CPO’s CDR and the eMSP’s session don’t reconcile. The cpo emsp settlement decisions an operator makes at this layer compound for the life of every roaming contract signed.

Cross-network EV roaming patterns walk through the protocol-side topology; the role-and-revenue question is what the operator captures or pays away at that topology. The Open Charge Alliance defines the protocol; the EVRoaming Foundation defines the operational baseline for hub and bilateral integration. The 2026 capability-audit companion covers the settlement and compliance capability gates the platform has to clear at this layer; the engineering-decision companion covers the API and event-bus architecture that makes the OCPI surface auditable. C18’s lane is the business consequence: who gets the basis points, and how does the integrated-stack operator capture the arbitrage at the OCPI settlement surface?

When the Operator Has to Run Both — and What CPO and eMSP Joint Solutions Actually Means

The 30-monthly-volume query cpo and emsp joint solutions is the operator looking for the integrated-stack guide. The current SERP does not deliver it. Three operator profiles where the integrated stack is becoming the right answer in 2026, not the exotic one:

The first is the utility-affiliated operator with regulated grid-services revenue. Utilities running V2G pilots, DR enrollment, or ancillary services need control of both the physical charger (CPO side) and the driver enrollment workflow (eMSP side) to deliver the grid-services product end-to-end. The integrated stack captures the value chain that the disaggregated model splits across vendor contracts. FERC Order 2222 in the US and the EU CER aggregation framework make this profile the leading edge of the integrated-stack adoption curve.

The second is the fleet operator with private depots and a branded driver app. The asset side is mandatory — fleets need predictable depot charging at predictable cost — and the driver side is the brand differentiator (fleet driver app, in-vehicle charging guidance, expense management). Running CPO + eMSP under one platform avoids the contractual seams between fleet asset operations and driver software. The same logic applies to large retail real-estate holders deploying private + public charging on the same site.

The third is the automaker-affiliated MSP with a proprietary charging network. Premium-segment driver retention depends on the unbroken experience — the brand owns the app, the network, the certificate-authenticated session, and the settlement workflow. The disaggregated model leaks brand surface to third parties. The integrated stack keeps the experience under one operator. ISO 15118-20 plug-and-charge spanning both layers makes this profile structurally more important than it was in 2023.

The implementation architecture for cpo and emsp joint solutions is one operator-owned platform spanning OCPP (charger control) plus OCPI (driver session routing) plus identity, settlement, billing, and driver app on top. The codebase is the asset. The eMSP Engine accelerator path is the implementation reference for the integrated-stack build; it ships the OCPI 2.2.1 baseline + plug-and-charge plumbing as a perpetual-license code base, compressing the integrated-stack calendar from 12-18 months to roughly 3-4. Operators evaluating the role-by-role build path can also reference the white-label evaluation guide for the first-market-entry path on the eMSP side; the integrated build path supersedes white-label once the operator commits to running both roles internally.

| Operator profile | Primary asset base | Revenue mix (CPO / eMSP) | Forcing functions binding first | Recommended platform path |

|---|---|---|---|---|

| Utility-affiliated operator | Existing grid infrastructure, regulated rate base, ratepayer-funded site portfolio | Mixed: energy spread + demand-charge management + DR/V2G + driver enrollment + grid-services billing | FERC Order 2222 (US ISO-RTO markets); EU CER aggregation framework; AFIR cross-role data publishing | Integrated stack from day one — value chain captured end-to-end; accelerator-led build compresses calendar to 3-4 months |

| Fleet operator with private depots | Private depot real estate, fleet operations, driver community | CPO-weighted (energy spread + utilization) with branded eMSP layer for fleet drivers | ISO 15118-20 plug-and-charge (depot + driver-vehicle handshake); AFIR (if any depot opens to public) | CPO-first build with integrated eMSP layer; the asset side is mandatory, the driver layer is the brand differentiator |

| Automaker-affiliated MSP | Driver relationship (vehicle owners), brand surface, proprietary charging network | eMSP-weighted (subscription + per-session commission + partnership revenue) with CPO layer for proprietary network | ISO 15118-20 plug-and-charge (premium-segment driver experience); AFIR (if branded network includes public sites) | eMSP-first build with integrated CPO layer once proprietary network reaches utilization threshold; brand requires unbroken experience under one stack |

The Role Question Is the First Question, Not the Last

The five sections above are the decision framework; the way to use it is the audit operators should run before committing capital. Most platforms shipped to a 2022 single-role spec are now playing catch-up against a 2026 forcing-function set that no longer respects the role boundary. Operators who picked eMSP-only or CPO-only at the start often discover the other role becomes mandatory at month eighteen — at which point the platform retrofit cost is materially higher than the planned-from-the-start integrated path.

The audit before committing has three questions. Which role’s revenue model fits the existing asset base? Which role’s forcing functions bind first in the target market? And does the second role become mandatory inside the 24-month strategy horizon? Operators who answer “yes” to the third question stop running emsp vs cpo as a binary choice and start running cpo and emsp as a sequenced commitment with one platform spanning both.

The 2026 Cluster 6 decision surface assembles into a coherent operator workflow: the four-lever investment thesis sets the strategic frame, the capability-audit checklist confirms the platform meets the 2026 forcing functions, and the engineering-decision deep dive confirms the codebase will scale past the third year. C18 sits in front of all three: the role-and-revenue decision that decides which lever, which capability category, and which engineering surface matter for the operator’s specific stack. For operators pursuing the integrated-stack build, the custom eMSP platform engagement lives in that lane; for operators accelerating phase-one production on the protocol baseline, the eMSP Engine accelerator path compresses the calendar without conceding ownership of either role’s capability surface.

| Operator archetype | Existing asset base | Recommended starting role | Likely second-role trigger | Trigger timeline |

|---|---|---|---|---|

| Utility-affiliated operator | Grid infrastructure + regulated rate base | Both from day one (integrated stack) | FERC 2222 / EU CER pilot moves from optional to mandatory in target ISO-RTO or member state | Already binding in 2026 leading markets; expanding 2027-2028 |

| Fleet operator with private depots | Fleet + depot real estate | CPO first | Driver-app retention or competitive fleet-management offering requires branded eMSP layer | ~12-18 months post depot rollout |

| Automaker-affiliated MSP | Vehicle owner relationship + brand | eMSP first | Premium-segment driver retention demands proprietary charging network (CPO role) | ~18-24 months post eMSP launch |

| Large retail / real-estate holder | Site portfolio + customer foot traffic | CPO first | Customer loyalty integration and branded payment require eMSP layer | ~18 months post charger deployment |

| Mobility app / branded EV program | Driver-side app + payment relationship | eMSP first | Network reliability demands operator-controlled charging assets (CPO role) in priority markets | ~18-24 months post platform launch |

Frequently Asked Questions

The CPO (Charge Point Operator) operates the physical charging hardware, site operations, energy procurement, OCPP-side charger control, and depot logistics. The eMSP (e-Mobility Service Provider) operates the driver relationship: identity, roaming credentials via OCPI, billing visibility, in-app experience, and support workflow. The emsp cpo difference is fundamentally a role-and-revenue distinction — the CPO captures asset-side margin (energy spread, utilization, demand-charge management, ancillary grid services); the eMSP captures driver-side margin (subscription, per-session commission, ad-hoc payment uplift, partnership revenue). The two roles settle their respective revenue lines at the OCPI 2.2.1 contractual surface. For the role-level explanation that precedes this decision framework, see the eMSP role definition; for the CPO-side platform companion, see the CPO-side platform companion.

The eMSP business model runs on driver-side revenue: subscription margin (B2C and B2B fleet), per-session commission on roaming sessions, ad-hoc payment uplift driven by AFIR’s mandatory contactless payment without account creation, and partnership revenue with corporate fleets, automaker programs, and utility-affiliated branded programs. The CPO business model runs on asset-side revenue: energy spread between wholesale procurement and retail tariff, utilization economics (revenue per kWh per station per day), demand-charge management in US ISO-RTO markets, and ancillary grid services including DR enrollment, V2G dispatch, and frequency response. The two revenue lines meet at the OCPI settlement surface where eMSPs pay CPOs per kWh dispensed plus per-session fees; the integrated operator captures both lines internally and captures the basis points the disaggregated model pays away.

Yes, and increasingly common in 2026. Three operator profiles where the integrated stack is the right answer: utility-affiliated operators with regulated grid-services revenue, fleet operators with private depots plus branded driver apps, and automaker-affiliated MSPs with proprietary charging networks. The integrated stack captures arbitrage at the OCPI settlement layer that the disaggregated model cannot — for operators in markets where the revenue models meet (UK, NL, DE, US ISO-RTO pilots), running both roles is moving from optional to structurally advantageous. The platform architecture for the integrated stack is one operator-owned codebase spanning OCPP, OCPI, identity, settlement, billing, and driver app on a single platform.

cpo and emsp joint solutions is the practical name for integrated-stack platforms that combine charge-point management (OCPP, telemetry, maintenance, energy procurement) with driver-side eMSP functions (identity, roaming, billing, in-app experience) on one operator-owned platform. The architecture is driven by four 2026 forcing functions pulling the roles together: AFIR enforcement imposes cross-role data and payment obligations; OCPI 2.2.1 hub maturity raises the depth bar on the contractual surface between the two; V2G market entry requires both physical asset control and driver-side settlement on the same transaction; FERC Order 2222 and the EU CER aggregation framework position the integrated operator as a potential aggregator counterparty in wholesale markets. The implementation reference is the eMSP Engine accelerator path, which ships the OCPI 2.2.1 baseline plus the ISO 15118-20 plug-and-charge plumbing as a perpetual-license codebase.

The answer depends on the operator’s existing asset base and revenue model. Operators with existing physical infrastructure (utilities, fleets with private depots, large retail real-estate holders) typically start with the CPO role and add eMSP capabilities once the network has driver traffic. Operators with existing driver relationships (automakers, mobility apps, branded EV programs, utility-affiliated programs) typically start with the eMSP role and add CPO capabilities once the brand needs proprietary charging infrastructure. Both paths converge by month eighteen for any operator competing in markets where the revenue models meet — at which point the second role’s capabilities become mandatory and the platform either supports both roles natively or requires a retrofit that costs materially more than the integrated build path would have cost in phase one.