EV Fleet Charging Software: The Operations Layer That Decides Depot Economics

EV fleet charging software is the part of fleet electrification nobody budgets for properly, and the part that ends up deciding cost per mile. The pattern is consistent on both sides of the Atlantic: a fleet commits to electrification, procures vehicles, procures chargers, and treats the software as a line item that comes with the hardware. Then the first winter quarter arrives. Trucks queue for plugs at 5 PM, the site hits its demand peak exactly when energy is most expensive, two chargers fault overnight with nobody alerted, and a vehicle leaves at 6 AM with 60 percent state of charge on a route that needs 80. None of those are charger problems. Every one of them is a software problem, and charging is a logistics problem before it is an energy problem.

Key Takeaways

- Chargers are capex with a known price; charging operations are an ongoing cost curve, and software is the only lever that bends it.

- Generic charging tools manage sessions. Fleet charging software manages departures: state of charge by route, by vehicle, by deadline, inside a fixed power envelope.

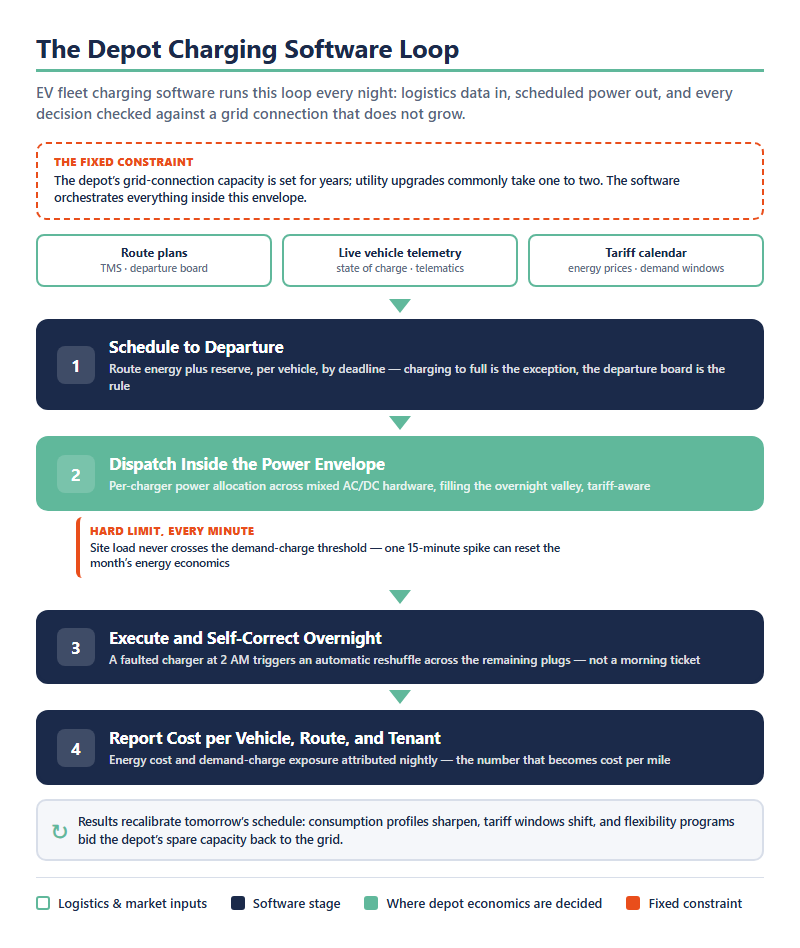

- The depot’s grid connection is the real constraint. Utility upgrades commonly take one to two years, so the practical question is how much fleet you can charge inside the capacity you already have.

- Charging as a service trades capex for a per-mile fee and someone else’s roadmap. At multi-depot scale, owning the software stack is usually where the economics flip.

Fleets Shop for Charging Solutions and End Up Needing EV Fleet Charging Software

Search behavior tells the story: operators look for EV fleet charging solutions, a phrase that suggests a single purchasable thing. What the market sells under that label is hardware plus installation plus a network subscription. What an operating fleet actually runs on, eighteen months later, is the software layer: the system deciding which vehicle charges when, at what power, against which tariff, and whether the morning departure board is green or red.

The distinction matters because the two purchases fail differently. Undersized hardware is visible in the business case before signature. Undersized software is invisible until operations start, because the gap only appears when route schedules, driver behavior, tariff windows, and site power limits interact. End-to-end depot charging solutions that bundle all of it exist, and for a first site they can be the right call. But the bundle’s software tier is where corners get cut, and it is the tier that determines whether the second and tenth sites inherit a platform or a problem. Fleets that separate the two questions, what hardware do we need and what software will operate it, consistently make better decisions on both; our work on EV fleet management solutions sits exactly at that second question.

The European version of this lesson is arriving through the logistics real-estate market. Depot owners electrifying multi-tenant fulfillment sites are discovering that the asset they are really building is not a row of dispensers; it is a charging operation their tenants’ delivery schedules depend on, with the Alternative Fuels Infrastructure Regulation (AFIR) raising the baseline for what public-facing charge points must support. The owners who treat that operation as software infrastructure are the ones able to offer charging to tenants as a product instead of a cost recovery exercise.

Why Generic Charging Management Tools Break at the Depot Gate

Plenty of competent platforms can start a session, bill it, and show a dashboard. Depot charging fails them on a different exam. A fleet depot is not a collection of charging sessions; it is a nightly logistics operation with an energy constraint. The software jobs are specific, and most general-purpose tools were never built for them.

| The job | Generic charging management answer | EV fleet charging software answer |

|---|---|---|

| Charge target | Charge to full when plugged in | State of charge by departure time: route energy plus reserve, per vehicle, per deadline |

| Scheduling input | Driver plugs in; session starts | Route plans from the TMS, live telematics state of charge, per-vehicle consumption profiles, tariff calendar |

| Site power limit | Static per-charger caps, if any | Dynamic orchestration of the whole depot inside the grid-connection envelope, tariff-aware |

| Charger fault at 2 AM | Alert ticket for the morning shift | Automatic schedule reshuffle across remaining chargers; departure board stays green |

| Hardware scope | Single vendor or certified list | Mixed AC/DC, multi-vendor fleets over open protocols |

| Cost reporting | Sessions and kilowatt-hours billed | Energy cost per vehicle, per route, per tenant; demand-charge exposure tracked nightly |

The defining job is charging to departure, not charging to full. A delivery van leaving at 6:40 AM on an 80-kilometer route does not need 100 percent state of charge at midnight; it needs its route energy plus reserve by 6:30, at the lowest possible energy cost, without pushing the site over its demand threshold. Solving that requires data generic tools never see: route plans from the transport management system (TMS), live state of charge from vehicle telematics, per-vehicle consumption profiles, and the tariff calendar. Fleet ev charger management software earns its name when it closes that loop automatically every night, across mixed AC and DC hardware from more than one vendor, and degrades gracefully when a charger faults at 2 AM by reshuffling the schedule instead of waking an operator.

This is also where fleet charging management stops being an energy discipline and becomes an integration discipline. Telematics platforms, TMS, charger fleets, building systems, and utility programs each speak their own protocol, and the most common failure mode we see in rescue engagements is a stack of point integrations that worked at ten chargers and collapsed at a hundred. The integration architecture, not the optimization math, is usually what separates a pilot from a platform.

The Power Envelope Is the Budget: Infrastructure, Demand Charges, and the Grid Connection You Have

Every depot has a number that matters more than its charger count: the capacity of its grid connection. EV fleet charging infrastructure is routinely planned as if that number were negotiable on a project timeline. It is not. Utility interconnection upgrades commonly run one to two years in both U.S. and EU markets, which the National Renewable Energy Laboratory’s fleet electrification research identifies as a central constraint on depot buildout. For most fleets, the honest planning question is therefore inverted: not how much capacity the full fleet needs, but how much fleet the existing capacity can charge if the software orchestrates it intelligently.

Orchestration inside the envelope is mostly arithmetic, relentlessly applied. Fifty trucks arriving between 5 and 7 PM do not need simultaneous full-power charging; they need a schedule that fills the overnight valley, respects every departure deadline, and never lets site load cross the threshold where demand charges reset the month’s economics. Load management at the charger level is the foundational mechanism here, and how network operators implement it is covered in our guide to EV charging load management; at the depot level the same mechanism gets composed with routes, tariffs, and departure boards into something closer to production planning.

The envelope also has a supply side. Depot charging increasingly co-locates with rooftop solar and on-site batteries, which can raise effective capacity without touching the interconnection, but only if the charging schedule and the energy assets are co-optimized rather than separately managed. The architecture for integrating depot charging with solar and on-site storage is its own discipline, and it is the natural second phase for sites that hit their grid ceiling early.

Managed Charging Turns the Depot from a Load into an Asset

A depot that can shape a megawatt of overnight load is interesting to its utility, and that interest is increasingly monetizable. Managed charging, the practice of letting price signals or utility programs steer when and how hard vehicles charge, is the fleet-scale version of a deal: flexibility in exchange for lower effective energy cost. U.S. utilities run managed-charging programs precisely because depot loads are large, predictable, and software-controllable; EU logistics sites face the same logic through time-varying tariffs and grid-services markets.

The software requirement is what distinguishes EV fleet managed charging software from a smart thermostat analogy: the fleet cannot simply curtail. Every flexibility decision has to be checked against tomorrow’s departure board, which means the platform must co-optimize three objectives at once: route readiness, energy cost, and program revenue. Done well, the depot’s flexibility becomes a revenue line. The same charger fleet that strains the site at 5 PM is, an hour later, a dispatchable resource, part of the broader pattern of charging flexibility revenue that operators are learning to capture. Vehicle-to-grid sits on the horizon of the same curve, and the fleets positioned to capture it will be the ones whose software already treats the depot as a controllable energy asset rather than a dumb load.

Charging as a Service or Owning the Stack: The Fleet Operator’s Real Build-Buy Map

Fleet charging as a service (CaaS) is the market’s answer to a real objection: fleets are logistics experts, not energy engineers, and many would rather pay per mile or per kilowatt-hour than build a charging operation. Under a CaaS contract, a provider finances, installs, and operates the depot, and the fleet buys an outcome: charged vehicles. For a first depot, a hard sustainability deadline, or a fleet that never intends to own energy operations, that trade is often right.

| Dimension | Charging as a service (CaaS) | Owning the software stack |

|---|---|---|

| Upfront cost | Minimal: provider finances hardware and operations | Capex plus a platform build or integration program |

| Unit economics at scale | Per-mile or per-kWh fees compound across depots | Cost per depot falls as the platform amortizes |

| Operational data | Accrues to the provider’s platform | Accrues to the fleet; portable and analyzable |

| Roadmap control | Vendor decides supported devices, tariffs, programs | Fleet prioritizes its own integrations and markets |

| Time to first depot | Fastest: outcome bought, not built | Slower start; accelerator-based builds compress it |

| Best fit | First site, hard deadline, no energy-ops ambition | Multi-depot or multi-country scale; data and flexibility revenue as strategy |

The trade has a slope, though. Per-unit pricing that looks reasonable at one depot compounds across fifty; operational data accrues to the provider’s platform rather than the fleet’s; and the roadmap, which devices, which tariff logic, which utility programs, moves at the vendor’s pace. Somewhere between the second depot and the second country, most large operators rediscover the build-versus-buy question, and the answer is rarely all-or-nothing. The workable pattern is owning the orchestration layer, the scheduling logic, integrations, and data, while still buying hardware, installation, and even financing as services. That is the architecture behind the fleet charging platform Codibly built for a global technology provider: hardware-agnostic control across multi-vendor chargers, automated load shedding for utility demand response, and a multi-tenant design that lets one platform serve many sites and operators. Owning that layer is also what keeps options open at the edges of the business, like monetizing idle fleet hubs by opening private infrastructure to outside drivers when the depot’s own vehicles are on the road.

The evaluation criteria, whichever side of the map a fleet lands on, are stable: route-aware scheduling depth, multi-vendor hardware support, telematics and TMS integration, load management inside a fixed envelope, utility-program readiness, and an exit path for the data. A provider or platform that clears those six is a real candidate. One that demos a dashboard is not.

The Fleet That Hits Cost-Per-Mile Targets Is Running Better Software, Not More Chargers

Electrification economics get decided in the gap between two numbers: what the depot pays for energy and what it would pay if every kilowatt-hour were drawn at the wrong time. Hardware cannot close that gap; it sets the ceiling, and the software decides how much of the ceiling converts into operating margin. The fleets and depot owners treating EV fleet charging software as core operational infrastructure, scoped with the same seriousness as the vehicles, are the ones hitting cost-per-mile targets while their grid connections stay unchanged. The energy transition needs electrified logistics at scale, and at scale, charging is software.

Frequently Asked Questions

EV fleet charging software is the operations platform that manages charging for a fleet of electric vehicles: scheduling each vehicle to reach its required state of charge by departure time, distributing limited site power across chargers, integrating telematics and route data, and reporting energy costs. It sits above the chargers themselves and below the logistics systems of the fleet, connecting both.

Managed charging steers when and how fast vehicles charge in response to energy prices, utility programs, or grid signals, instead of charging every vehicle at full power on arrival. For fleets it always operates under a readiness constraint: cost and flexibility are optimized only within schedules that guarantee every vehicle meets its departure time and route energy requirement.

Fleet charging as a service (CaaS) is a commercial model in which a provider finances, installs, owns, and operates depot charging infrastructure, and the fleet pays per kilowatt-hour, per mile, or per vehicle for guaranteed charging outcomes. It compresses time-to-electrification and removes capex, in exchange for recurring per-unit costs, provider-held data, and a roadmap controlled by the vendor.

Test six capabilities: route-aware charging schedules driven by departure times and state of charge, multi-vendor charger support over open protocols, integration with telematics and transport management systems, load management that respects the power limit of the site, readiness for utility tariff and flexibility programs, and portability of your operational data. Pricing structure matters at scale: per-charger fees that work at one depot can become the dominant cost line across many.

Beyond vehicles and chargers, depot infrastructure includes the grid connection and any capacity upgrades, switchgear and distribution, optional on-site solar and battery storage, network connectivity, and the software layer that operates all of it. The grid connection is usually the binding constraint, which is why software-based load orchestration is treated as infrastructure rather than an accessory.