ERCOT Demand Response: ADER Pilot, ERS, LaaR & Software Architecture for Texas Aggregators

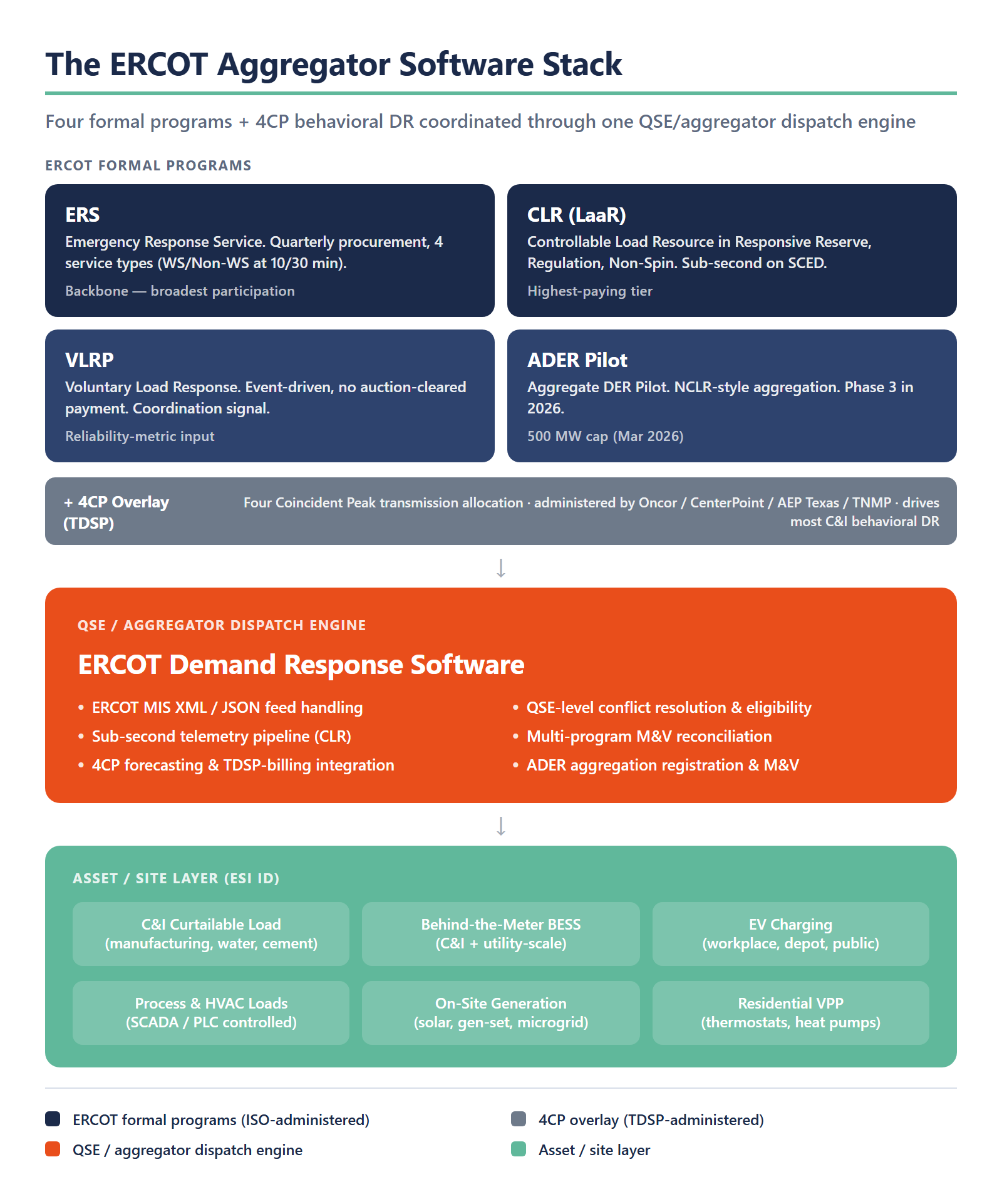

ERCOT is the most fragmented demand response market in the US. The same aggregator may simultaneously bid load into Emergency Response Service (ERS), Load Resources participating in ancillary services as Controllable Load Resources (LaaR/CLR), Voluntary Load Response (VLRP), and the Aggregate Distributed Energy Resource (ADER) Pilot — each with its own telemetry profile, settlement methodology, registration cap, and software interface. The pilot itself just expanded to a 500 MW Registered Capacity Limit in March 2026, which puts a real production VPP stack inside the formal ERCOT market for the first time. The 4CP transmission cost allocation operates on top of all of this and drives most C&I behavioral demand response in Texas. The aggregator software that wins ERCOT is the one that stacks across all four formal demand response aggregator business models and handles 4CP-driven C&I behavioral DR on the same control plane. This guide walks through the ERCOT demand response programs and the software architecture that participates.

Why ERCOT Demand Response Is Different — Energy-Only Market Design and What It Forces on the Software

ERCOT is an energy-only market. There is no formal capacity market like PJM Capacity Performance, ISO-NE FCM, or NYISO ICAP — which means revenue stacking for ERCOT demand response works fundamentally differently than every other US ISO. Aggregator software designed for capacity-market participation translates poorly to Texas, and aggregators that learned the trade in PJM demand response aggregator software routinely underbuild their ERCOT stack as a result.

The closest ERCOT analogue to a capacity-market mechanism is ERS, but it is procured quarterly through four standard contract terms and pays differently than PJM CP. The 4CP transmission cost allocation is the other revenue lever in Texas, and it is not an ISO program at all — it is a TDSP transmission cost allocation tariff that drives most C&I behavioral curtailment by allocating transmission charges based on a customer’s load during the four highest 15-minute system peaks of summer.

Why energy-only is the most consequential design choice for ERCOT software

Capacity-market revenue is annual, predictable, and pays for availability — the software optimizes for “show up when called.” Energy-only revenue is event-by-event, volatile, and pays for delivered MW — the software optimizes for “bid intelligently into a market that may or may not call you.” The two design philosophies pull software architecture in different directions.

Where the boundaries between ERCOT programs and TDSP tariffs are (and why software has to read both)

ERCOT runs the wholesale programs (ERS, LaaR/CLR, VLRP, ADER). The TDSPs (Oncor, CenterPoint, AEP Texas, TNMP) administer 4CP and certain emergency interruptible tariffs. Aggregator software that ignores the TDSP layer misses one of the largest C&I curtailment-revenue surfaces in Texas. This boundary is the same reason existing custom software for ERCOT REPs has to integrate against TDSP-side data, not just ERCOT MIS feeds.

ERS: The Backbone Program — Procurement, Service Types, and Software Stress Points

The ERCOT Emergency Response Service is the program every Texas aggregator builds for first because it is open to commercial, industrial, and residential participants and has the most procurement frequency. ERCOT procures ERS quarterly across four standard contract terms (December–March, April–May, June–September, October–November), and Resource Identification (ERID) information is due to ERCOT before each procurement window. Competitive offers and self-provision offers are submitted on published schedules, and pricing clears at the ERS auction.

There are four ERS service types — Weather-Sensitive ERS-10, Non-Weather-Sensitive ERS-10, Weather-Sensitive ERS-30, and Non-Weather-Sensitive ERS-30. The 10 and 30 refer to maximum response time in minutes. Weather-Sensitive ERS pays more but only deploys during specific weather conditions; Non-Weather-Sensitive deploys based on grid stress regardless of weather. The software stress points fall on the 10-minute service types: real-time telemetry SLA, certified protocol-stack adapters, and an audit trail that survives a non-performance dispute.

| Service type | Max response time | Typical revenue | Telemetry & software requirements |

|---|---|---|---|

| WS ERS-10 (Weather-Sensitive) | 10 minutes | Highest of the four; weather-dependent activation pays a premium for the matching reliability profile. | Sub-minute telemetry, certified protocol-stack adapters, audit-grade logging. The hardest ERS tier to deliver and the highest ERID qualification bar. |

| Non-WS ERS-10 (Non-Weather-Sensitive) | 10 minutes | Above the 30-minute tiers; pays for unconditional 10-min availability under any grid-stress trigger. | Same telemetry and reliability bar as WS-10; broader event-trigger logic in the dispatch engine. |

| WS ERS-30 (Weather-Sensitive) | 30 minutes | Lower than the 10-minute tiers; weather-conditional activation. | Minute-scale telemetry acceptable; standard CBL-style M&V; software floor much lower than the 10-min tiers. |

| Non-WS ERS-30 (Non-Weather-Sensitive) | 30 minutes | Lowest of the four; the entry-point tier most aggregators build for first. | Minute-scale telemetry, standard M&V, ERID registration. Where the on-ramp to ERCOT DR usually starts. |

The 30-minute service types are easier to deliver but pay less per MW; the 10-minute types are where margin lives but require sub-minute telemetry and reliability discipline most aggregators underestimate.

LaaR / Controllable Load Resource: Ancillary Services Participation and Sub-Second Software

Load Resources participating in ancillary services — historically called LaaR, formally now Controllable Load Resources (CLR) — are the highest-paying ERCOT DR program but the hardest to qualify for. CLRs participate in Responsive Reserve, Regulation Service (Up and Down), and Non-Spin, and they dispatch on ERCOT’s 5-second SCED granularity. The qualification process is rigorous: site-level metering certification, QSE registration, telemetry pipeline acceptance testing, and AS-eligible site qualification.

Software requirements for CLR are an order of magnitude more demanding than ERS. The telemetry pipeline must deliver sub-second readings to ERCOT’s MIS; the dispatch engine must respond to AS deployment signals on the SCED cycle; the M&V baseline methodology must hold up under audit because penalties are steep and the AS market is unforgiving. Most aggregator stacks built for ERS can be extended to ERS-30 with modest engineering; adding CLR is a different kind of software project. The pattern is closer to building automated demand response programs for ancillary-service grade signals than to extending an emergency-response stack.

Why CLR is harder to build than ERS but pays more per MW

Responsive Reserve and Regulation Service pay continuously across the year — not only during procurement-window events. The MW-hour math is fundamentally better than ERS, but the software floor is higher. Aggregators that build the CLR stack right capture the most lucrative MW in ERCOT; aggregators that try to bolt it onto an ERS-grade platform burn quarters of engineering and routinely fail certification.

VLRP and 4CP-Driven Behavioral DR: The Two Programs That Don’t Show Up in Aggregator Software RFPs

ERCOT’s Voluntary Load Response Program is event-driven and ad-hoc — ERCOT calls it when grid conditions warrant, participants curtail voluntarily, and there is no auction-cleared payment. VLRP shows up as the third or fourth bullet on every ERCOT DR overview deck and rarely shows up in aggregator software RFPs because the revenue mechanics are weaker than ERS or CLR. But the software still has to handle it — VLRP performance feeds into ERCOT’s reliability metrics and informs ERS and CLR procurement preferences in subsequent windows.

The bigger software-blind-spot in ERCOT is 4CP-driven behavioral DR. 4CP — the four coincident peak transmission cost allocation — is administered by the TDSPs (not ERCOT), and the dollars at stake for a large C&I customer can be larger than any ISO program revenue. The 4CP mechanism allocates transmission charges based on a customer’s load during the four highest 15-minute system-wide peaks of June–September. Avoiding load on those four intervals can cut transmission charges materially. C&I customers with on-site flexibility (BESS, EV charging, controllable HVAC, process curtailment) chase the 4CP signal aggressively; the software that does it well looks like a demand side response platform architecture guide more than like a traditional DRMS.

Why C&I sites under 4CP-driven curtailment look like flexibility but settle outside formal programs

The aggregator software has to read TDSP load data, forecast the four likely 4CP intervals (a probabilistic problem each summer), dispatch curtailment, and reconcile against TDSP transmission billing — none of which involves ERCOT MIS. This is the surface where commercial & industrial demand response software has the most leverage in Texas, and it sits entirely outside the formal program stack.

VLRP as the bridge between formal programs and ad-hoc utility coordination

When ERCOT issues a VLRP call, well-architected aggregator software treats it as a coordination signal across all enrolled assets — even those participating primarily in ERS or CLR — to bias toward voluntary curtailment without breaking program-specific obligations. The bridge is operational, not contractual.

The ADER Pilot in 2026: Phase 3, the 500 MW Cap, and What VPP Aggregators Build Now

The ERCOT Aggregate Distributed Energy Resource Pilot is the freshest software opportunity in Texas DR. The pilot has moved through phases since 2022 — Phase 1 launched at 40 MW, Phase 2 at 80 MW, Phase 3 (2025) doubled to 160 MW with an “NCLR-style” participation model that broadened access to ancillary services. ERCOT’s March 2026 Market Notice M-A030226-01 raised the Registered Capacity Limit to 500 MW and the QSE Limit from 50% to 90%. As of December 2025, seven commercial ADERs were participating, up from three in mid-2025; February 2026 ERCOT data showed three VPPs providing 25.5 MW of energy plus nearly 20 MW of other reserve services.

The path to permanent market integration is now visible. ERCOT’s pilot governing document gives the operator discretion to raise participation limits as registered capacity approaches the cap, and the March 2026 increase reflects exactly that — the program is succeeding in attracting commercial ADERs faster than the original cap structure anticipated. Aggregator software being built for ADER Phase 3 is the software that will participate in the permanent ADER program when ERCOT’s market rules accommodate it formally.

How ADER’s NCLR-style participation model changes the software requirement vs LaaR

NCLR-style participation lets aggregators bring DERs of mixed types under a single ADER, register at the QSE level, and bid into ancillary services without each individual DER needing CLR-grade certification. The software trade-off is that the aggregator now owns the verification — telemetry, baseline, audit — that ERCOT used to verify per-site under traditional CLR. The aggregator software has to be production-grade about M&V at the aggregation level. This is the same operational shape as the demand response management system stack used in PJM and ISO-NE, adapted to ERCOT’s settlement.

The path to permanent market integration — what aggregators are building for now

The pilot is an operating window for software that will compete for the post-pilot permanent program. Aggregators on the right side of this window have production VPPs running today; aggregators on the wrong side are still in due-diligence on the pilot. The competitive ranking after permanent integration will reflect that gap.

Stacking Programs: How an ERCOT Aggregator Builds Software That Participates in All Four

The hard part of ERCOT demand response software is not any single program — it is operating four formal programs (ERS, CLR, VLRP, ADER) plus 4CP-driven behavioral DR simultaneously on the same platform. On a hot August afternoon, an aggregator may face an ERS event, an ADER call, a 4CP-likely interval, and CLR Responsive Reserve dispatch within a one-hour window. Conflict resolution is operational, not theoretical.

Software has to handle QSE-level conflict resolution (a single QSE may run sites enrolled in multiple programs); per-site eligibility logic for stacked enrollments (CLR sites cannot also be in some ERS service types); settlement reconciliation across four programs plus TDSP 4CP billing; and forecasting that biases dispatch ordering toward maximum revenue across the stack rather than per-program optimization. The verbatim phrase “ercot demand response programs” describes the four formal stacks; “4CP-driven behavioral DR” is the fifth surface that lives in TDSP territory.

| Program | Simultaneous eligibility with other ERCOT programs | Settlement separation | Software stress point |

|---|---|---|---|

| ERS (all four service types) | Compatible with VLRP and 4CP-driven C&I curtailment. CLR-enrolled sites have program-level restrictions; ADER aggregations may include former ERS sites under different registration paths. | Quarterly auction settlement; clean separation from real-time energy market revenue. | Real-time telemetry SLA on the 10-min service types; non-performance penalty audit trail. |

| CLR (LaaR) in Responsive Reserve / Regulation / Non-Spin | Site-level CLR enrollment is not stackable with ERS for the same site; the QSE may run different sites in each program. | Continuous AS market settlement at 5-second SCED granularity; separate from energy market. | Sub-second telemetry pipeline; SCED-cycle dispatch latency; M&V baseline that survives audit. |

| VLRP | Compatible with all other programs; voluntary participation does not trigger formal eligibility conflicts. | No auction-cleared payment; performance feeds into reliability metrics that inform future ERS / CLR procurement preferences. | Coordination-signal handling across enrolled assets; not a primary revenue stack. |

| ADER Pilot (Phase 3, 500 MW cap as of Mar 2026) | NCLR-style aggregation under a single QSE; mixes asset types that would not individually qualify for CLR. Not stackable with site-level CLR for the same physical assets. | Pilot-specific settlement structure; aggregation-level M&V rather than per-site. | VPP control-plane abstraction; multi-OEM device coordination; aggregation-level M&V audit. |

| 4CP-driven C&I behavioral DR (TDSP-administered) | Compatible with all ERCOT programs at the site level; runs entirely outside ERCOT MIS feeds and settlement. | Annual transmission-charge avoidance billed via TDSP; not visible in ERCOT settlement at all. | Probabilistic 4CP-interval forecasting; TDSP-side data integration; transmission-billing reconciliation. |

The stacking matrix is operational guidance, not a regulatory rulebook — ERCOT and TDSP rules evolve, and software has to encode the rules as configuration, not hard-coded logic.

ERCOT Aggregator Software: Build vs Buy vs Accelerator-Led Selection Criteria

The procurement decision for an ERCOT-focused aggregator falls along six criteria. Most aggregator software platforms underdeliver on at least three.

- ERCOT API integration certification. ERCOT MIS XML/JSON feeds, ESI ID-level telemetry routing, QSE registration management, and ERS submission workflows. The phrase “ercot public api integration complexity” is real — Codibly’s GSC data shows the query lands on the DR program integration services page at position 7.7, which suggests the buyer is searching for software that solves it.

- Sub-second telemetry pipeline for CLR. Kafka or MQTT with backpressure handling, durable replay, and end-to-end latency budgets that survive an SCED-cycle audit. Most cloud-native DRMS stacks struggle here because the telemetry was originally architected for hourly settlement.

- 4CP forecasting + dispatch automation. Probabilistic forecasting of the four coincident peaks, automated dispatch decision logic, and integration with TDSP transmission billing data. This is where C&I revenue lives and where most aggregator stacks have a hole.

- ADER QSE and aggregation registration. ADER-specific telemetry, settlement, and the aggregation-layer M&V required by NCLR-style participation. Worth engineering only for aggregators serious about the permanent post-pilot program.

- Multi-program M&V reconciliation. Customer Baseline Load methodologies for ERS, weather-normalized regression for some CLR participation, and aggregation-level M&V for ADER. Settlement reconciliation across all three is a real engineering project.

- TDSP coordination for C&I sites under 4CP. Reading TDSP transmission billing data, integrating with TDSP 4CP coordination interfaces, and operating across the Oncor / CenterPoint / AEP Texas / TNMP territory boundaries.

The ercot demand response software an aggregator buys or builds for these six criteria determines how much margin the aggregator extracts in Texas. SaaS platforms (demand response software & platform pillar covers the broader vendor landscape) cover ERS reasonably well and CLR partially; few cover 4CP or ADER credibly. Accelerator-led custom development through an OpenADR Accelerator path is the most common route for aggregators with multi-program ambitions.

The ERCOT Question Is The Multi-Program Stacking Question in Disguise

Every ERCOT aggregator software decision is a decision about how many of the four formal programs (plus 4CP-driven C&I) the platform can stack without breaking QSE eligibility, telemetry SLA, or settlement reconciliation. Energy-only market design rewards software that bids well, dispatches reliably, and settles cleanly across heterogeneous program mechanics — and Texas is the market where the aggregator software gap is widest because most off-the-shelf DRMS was built for capacity-market environments.

If you are scoping ERCOT DR program integration services — or evaluating capacity market integrations for the contrast with capacity-market ISOs — start by mapping which of the four formal ERCOT programs your portfolio participates in, which 4CP exposure you are managing for your C&I customers, and which ADER pilot path you are positioning for. The answer to the procurement question follows the answer to that map.

For the architecture-level companion piece on a real-time-dispatch platform that the same software has to deliver across multiple ISOs, see the demand side response platform architecture guide. For the demand response aggregator business models overview, see the cluster pillar.

Frequently Asked Questions

ERCOT demand response is the participation of Texas electricity loads in ERCOT-administered programs that pay for verified load reductions during specific events or windows. ERCOT runs four formal programs — Emergency Response Service (ERS), Load Resources participating in ancillary services as Controllable Load Resources (LaaR/CLR), Voluntary Load Response Program (VLRP), and the Aggregate Distributed Energy Resource (ADER) Pilot — plus 4CP-driven behavioral DR administered by Texas TDSPs. Combined, these surfaces represent the largest formal DR opportunity in any energy-only US market.

Four formal programs plus 4CP. ERS is procured quarterly with four service types (WS/Non-WS at 10/30-minute response). CLR participates in ancillary services (Responsive Reserve, Regulation, Non-Spin) on ERCOT’s 5-second SCED granularity. VLRP is event-driven voluntary curtailment without auction-cleared payment. ADER is the pilot for aggregator-led DER participation, expanded to a 500 MW cap in March 2026. 4CP is a TDSP transmission cost allocation that drives most C&I behavioral DR.

The ADER Pilot is ERCOT’s path for aggregators to bring distributed energy resources (BESS, controllable load, generators) under a single Aggregate Distributed Energy Resource and bid into the wholesale market. Phase 3 (2025) introduced an NCLR-style participation model and doubled the cap to 160 MW. ERCOT’s March 2026 Market Notice raised the Registered Capacity Limit to 500 MW and the QSE Limit from 50% to 90%. Seven commercial ADERs were participating as of December 2025. The pilot is on the path to permanent market integration once ERCOT’s market rules accommodate it formally.

The 4CP — Four Coincident Peak — is a TDSP transmission cost allocation methodology that bills C&I customers’ transmission charges based on their load during the four highest 15-minute system-wide peaks of June–September. Reducing load on those four intervals can cut transmission charges materially for the following year. 4CP is administered by the four TDSPs (Oncor, CenterPoint, AEP Texas, TNMP), not by ERCOT, but it is one of the largest demand-response revenue surfaces in Texas because it pays continuously through transmission-bill avoidance. Aggregator software that handles 4CP forecasting and automated dispatch captures revenue most ERCOT-centric platforms miss.

Yes — and most large C&I facilities in ERCOT participate in at least two of the five surfaces simultaneously. Manufacturing plants and water treatment commonly run ERS plus 4CP; data centers and large retail run 4CP plus VLRP; sites with significant on-site generation or storage may also enroll in CLR or ADER. The software that handles this multi-program participation looks like the architecture covered in the commercial & industrial demand response software guide, tuned for Texas program mechanics.