Virtual Power Plant Software: The Stack That Decides Which Aggregators Scale

The flexibility market is entering its most consequential phase on both sides of the Atlantic. In Europe, TSOs across Poland, Romania, Hungary, and Germany are shifting their balancing mechanisms toward real-time demand response and distributed storage. In the United States, FERC Order 2222 compliance filings are opening wholesale markets to aggregated distributed resources, and utility virtual power plant programs are moving from pilot to procurement. The window favors agile aggregators — and the companies winning it are rarely the ones with the sharpest trading strategies alone. They are the ones whose virtual power plant software can move faster than the grid itself.

For senior energy professionals who built their careers in commodity trading and flexibility origination, the technology question is often the last thing they want to deal with, and the first thing that limits their scale.

Key Takeaways

- VPP software has become the competitive moat in flexibility aggregation: the constraint on growth is how fast you can connect a new asset, market, or product — without rebuilding the platform.

- A production-grade VPP platform is four distinct technology layers, each with its own protocol demands; most teams under-scope at least two of them.

- Lean aggregators lose margin at integration points, not in trading strategy. A single TSO or ISO API integration costs 4–12 weeks of senior engineering time, and that debt compounds.

- Build versus partner is settled by talent scarcity and maintenance drag: protocol standards and market APIs change constantly, and pre-built accelerators convert that overhead into time-to-market.

From Trading Floor to Control Room: Why VPP Software Has Become a Competitive Moat

The thesis is now mainstream: flexible, algorithmically driven energy operators consistently outperform legacy structures. Poland’s PV capacity has grown from under 2 GW in 2019 to more than 23 GW. BESS deployment is accelerating across Central and Eastern Europe, and the planned phase-out of Russian gas imports by 2027 forces a step-change in demand-side flexibility at a scale manual trading strategies cannot service. The U.S. tells the same story with different drivers: the Department of Energy’s virtual power plant analyses point to tens of gigawatts of needed VPP capacity by 2030, and FERC Order 2222 gives aggregations a legal right to wholesale participation.

What separates aggregators who capture this opportunity from those who watch it pass is the quality of their software stack. Specifically: how quickly they can connect a new asset type, integrate a new market, and operationalize a new flexibility product — without rebuilding their core platform each time.

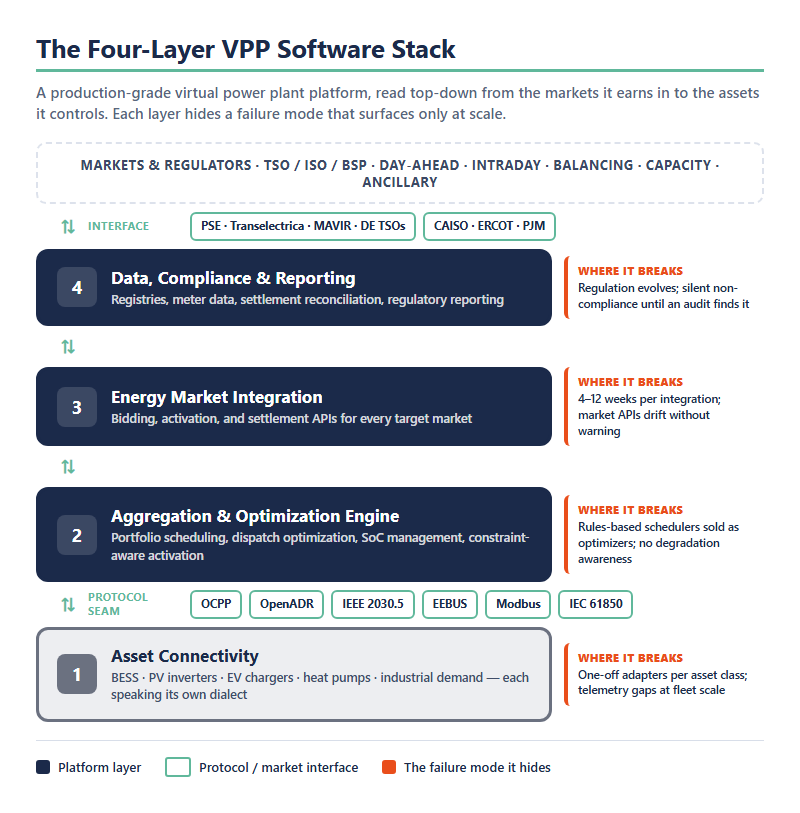

The Four Technology Layers Every Scalable VPP Platform Needs

A production-ready flexibility aggregation platform is not a single application. It is a stack of four distinct technology layers, each with its own protocol demands and integration complexity.

| Layer | The job | Protocols & interfaces | Where it breaks |

|---|---|---|---|

| 1. Asset connectivity | Reach every asset in real time, regardless of vendor | OCPP, OpenADR, IEEE 2030.5, EEBUS, Modbus, IEC 61850 | One-off adapters per asset class; telemetry gaps at fleet scale |

| 2. Aggregation & optimization | Portfolio scheduling, dispatch optimization, SoC management | Internal engine + asset constraint models | Rules-based schedulers sold as optimizers; no degradation awareness |

| 3. Energy market integration | Bid, activate, and settle in every target market | TSO/BSP APIs (PSE, Transelectrica, MAVIR, German TSOs), ISO market systems (CAISO, ERCOT, PJM) | 4–12 weeks per integration; APIs drift without warning |

| 4. Data, compliance & reporting | Registry connectivity, meter data, settlement, regulatory reporting | GO registries, MDM, market settlement formats | Regulation evolves (RED III, EMD, FERC 2222 filings); silent non-compliance |

1. Asset Connectivity Layer

Every asset in your portfolio — BESS units, PV inverters, industrial demand consumers, heat pumps, EV chargers — communicates through a different protocol. OCPP for EV charging infrastructure, OpenADR for demand response signaling, IEEE 2030.5 for utility-facing DER communication in U.S. programs, EEBUS for smart home devices, Modbus and IEC 61850 for industrial assets. Your connectivity layer must handle all of these in real time. Making heterogeneous assets reachable at fleet scale is a discipline of its own — the gateways, data models, and protocol seams covered in our guide to distributed energy resources integration.

2. Aggregation and Optimization Engine

Above the connectivity layer sits the logic that makes a VPP valuable: portfolio scheduling, dispatch optimization, state-of-charge management for storage, and constraint-aware activation across heterogeneous asset types. This is where algorithmic approaches create the most immediate advantage — optimizing dispatch sequences across hundreds of assets simultaneously against real-time market price signals. It is also where the VPP category borders DERMS software: a DERMS orchestrates resources for grid-operator objectives, while a VPP engine optimizes a portfolio for market revenue. The architectural decision between the two is mapped in our DERMS vs VPP comparison.

3. Energy Market Integration Layer

This is where most aggregators face their sharpest bottleneck. Each market — day-ahead, intraday continuous, balancing, capacity market, ancillary services, and in the U.S. each ISO’s participation model — requires a dedicated API integration with its TSO, ISO, or BSP. Across Poland (PSE), Romania (Transelectrica), Hungary (MAVIR), and Germany (all four TSOs), each has different data formats, authentication schemes, and submission windows; CAISO, ERCOT, and PJM repeat the pattern with their own market systems. Building and maintaining these integrations is a significant, ongoing engineering investment.

4. Data, Compliance, and Reporting Layer

The top of the stack handles everything regulators and counterparties require: GO registry connectivity, meter data management, settlement reconciliation, and cross-border or cross-jurisdiction reporting. As energy regulation evolves — RED III and the Electricity Market Design Regulation in Europe, FERC 2222 compliance filings and state program rules in the U.S. — this layer requires constant maintenance to remain compliant.

Where Lean Aggregators Lose Revenue: The Integration Gap

Most flexibility aggregators don’t lose margin in their trading strategies. They lose it at integration points.

Consider the actual cost of launching a new flexibility product in a new market: a single TSO or ISO API integration takes 4–12 weeks of senior engineering time. A new asset type requiring a new protocol adapter adds another 2–6 weeks. A regulatory compliance update — a change to Poland’s Capacity Market registration portal, a MAVIR ancillary service specification revision, an ISO market-system update — can freeze operations for days if integrations are brittle.

For a lean team of 5–15 people focused on trading strategy, origination, and deal execution, this integration debt accumulates faster than it can be serviced in-house. Every week spent on API maintenance is a week not spent on the next commercial opportunity. The economics of who captures aggregation margin — and how thin it runs when operations drag — are quantified in our analysis of demand response aggregator business models.

Large utilities absorb this cost with dedicated engineering departments. Independent aggregators competing against them need a different model.

Speed-to-Market Is the Real Competitive Advantage

In a balancing market, being three months late to connect means missing an entire seasonal price pattern. When a new ancillary service product launches — aFRR, mFRR, FCR, a DSR tender in Europe, or a new ISO pilot in the U.S. — the aggregators with pre-built integration infrastructure capture the first-mover premium. Those still building API connectors arrive to a flattened spread.

The same logic applies to asset onboarding. A flexibility aggregator who can onboard a new industrial demand consumer in two weeks rather than two months will consistently win origination mandates against competitors still assembling their Modbus integration.

This is why the most sophisticated flexibility operators are treating their aggregator and optimizer software stack as a strategic investment rather than an IT cost center. The ability to expand into a new country, asset class, or market product without rebuilding core infrastructure is the moat that compounds over time.

Build vs. Partner: The Real Economics for Flexibility Operators

The vendor landscape complicates the choice. Virtual power plant companies span three categories: hardware OEMs that embed aggregation features in their device ecosystems, aggregator-operators that run proprietary platforms, and software vendors that sell the stack as a product. Scanning lists of VPP companies rarely settles anything, because the decision that matters comes first: which parts of the stack to own.

Building a full VPP software stack in-house sounds appealing on paper. In practice, the hidden costs are substantial:

- Talent cost: Senior energy software engineers who understand both the protocol layer (OpenADR, OCPP, IEEE 2030.5, IEC standards) and energy market mechanics (balancing, ancillary services, capacity markets) are among the scarcest technical profiles on either continent.

- Protocol maintenance: Energy communication standards evolve constantly. OpenADR 2.0b to 3.0, OCPP 1.6 to 2.0.1 to 2.1, IEC 61850 profile updates — each requires dedicated engineering cycles to maintain compatibility.

- Market API drift: TSO and ISO APIs change without warning. A PSE balancing market portal update or a MAVIR capacity market specification revision is an operational blocker if not addressed immediately.

- Regulatory compliance overhead: Compliance across multiple jurisdictions requires ongoing legal and technical monitoring that most trading-focused teams are not structured to provide.

Partnering with a specialist who has already built — and actively maintains — pre-certified protocol accelerators and market integrations converts a capital expense into a time-to-market advantage. That is the model behind our energy market automation work for a European VPP provider, where WIRE, OTE, and HUPX trading integrations shipped as one engagement instead of three internal projects. For operators who need the platform itself — the optimization engine, the protocol layer, the market connectors — custom VPP development on accelerator foundations compresses each new market entry into months gained.

What This Means for BESS-Heavy Portfolios

Battery storage is increasingly the anchor asset in VPP portfolios on both continents — and the most demanding in terms of software requirements. A BESS asset participates simultaneously in day-ahead arbitrage, intraday balancing, FCR/aFRR or ISO ancillary services, and potentially capacity contracts. Orchestrating these concurrent obligations without conflicting dispatch commands requires a dispatch-grade BESS energy management system underneath the VPP layer — one that understands the asset’s technical constraints (SoC limits, ramp rates, cycle degradation) as well as the market context. The full control-stack anatomy, from cell-level firmware to market interface, is mapped in our analysis of energy storage software.

The aggregators building durable BESS portfolios are the ones who invested in this software layer early — before scale made the technical debt insurmountable.

The Aggregators That Scale Are the Ones That Stopped Rebuilding

Trading edge decays; integration capacity compounds. Every market the platform already speaks to, every protocol it already translates, every compliance format it already emits makes the next product launch cheaper than the last. That is the property that separates a flexibility business from a flexibility project — and it is decided in the software stack, usually two years before the difference shows up in the P&L. Operators who treat virtual power plant software as the business itself, not the plumbing under it, are the ones still in the market when the spread tightens.

Frequently Asked Questions

A virtual power plant (VPP) is a network of distributed energy assets — batteries, solar installations, EV chargers, controllable loads — aggregated and operated by software as a single dispatchable resource. The assets stay physically distributed; the software layer makes them behave like one power plant that can bid into markets, respond to grid signals, and balance supply and demand.

VPP software connects to each asset through its native protocol, aggregates real-time telemetry into a portfolio view, optimizes dispatch against market prices and grid signals, and sends control commands back to the assets. Revenue flows from energy arbitrage, balancing and ancillary services, capacity programs, and demand response — with the optimization engine deciding which asset serves which obligation at any moment.

Virtual power plant software is the four-layer technology stack that makes aggregation work: asset connectivity (protocol adapters), the aggregation and optimization engine, energy market integrations, and the data, compliance, and reporting layer. For flexibility aggregators, its quality determines how quickly they can onboard new assets, enter new markets, and respond to price opportunities.

A utility VPP program is a structured offering in which a utility enrolls customer-owned assets — typically batteries, smart thermostats, and EV chargers — and dispatches them for grid needs in exchange for incentives. U.S. programs have moved from pilots to standing procurement in several states, and FERC Order 2222 separately opens wholesale markets to aggregator-run VPPs independent of utility programs. Our dedicated guide to virtual power plant programs covers enrollment, compensation, and program design in depth.

A DERMS is grid-operator software for managing distributed resources to keep the distribution network stable; a VPP aggregates resources to participate in energy markets. Many deployments need both, and the boundary has architectural consequences — our DERMS vs VPP vs ADMS comparison on the Codibly blog maps the decision in detail.